A $13,500 robot is not a $13,500 worker.

The humanoid price crash is real. It is also the most misleading number in tech right now, because the scarcity already moved off the robot.

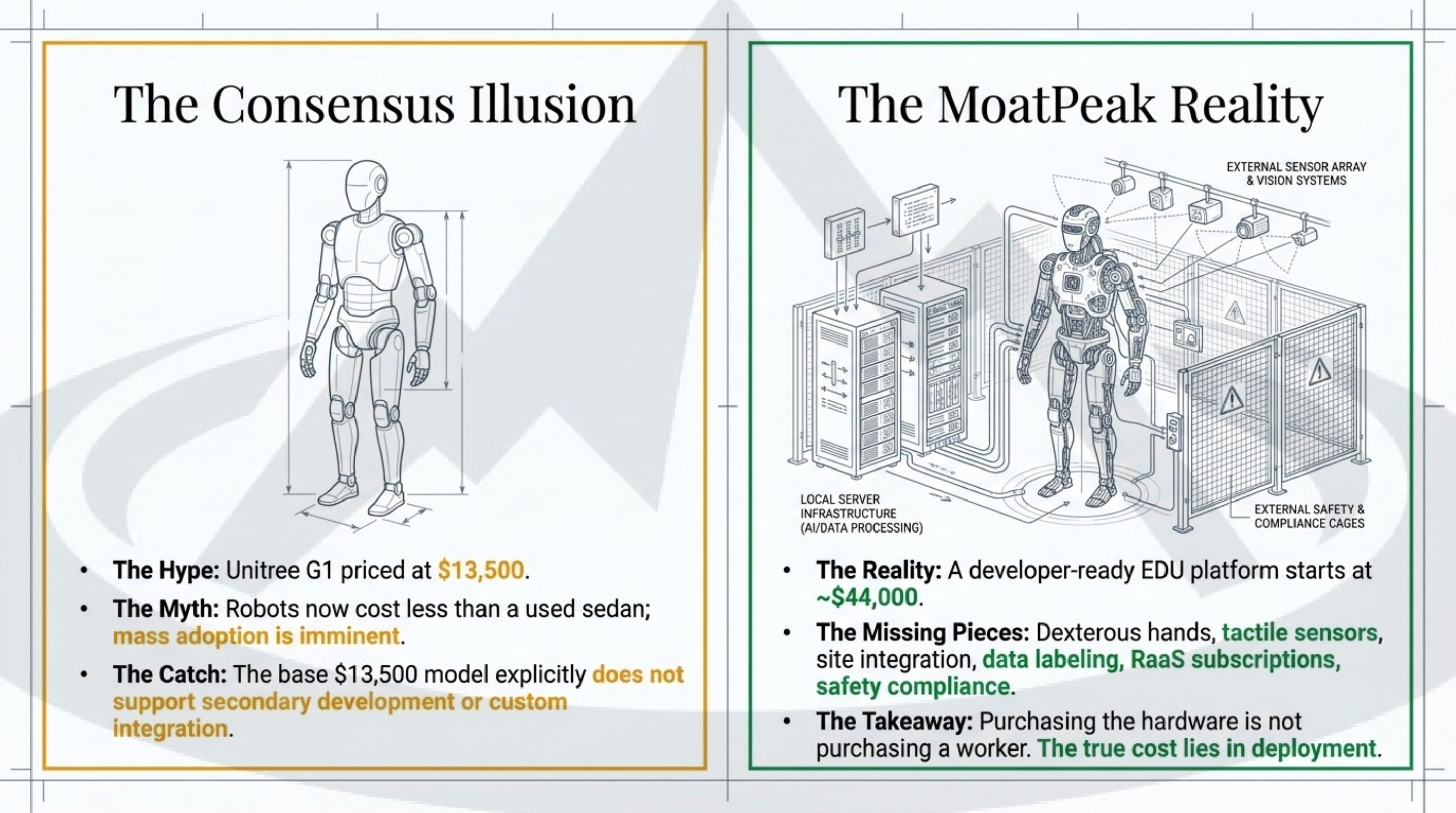

The cheapest humanoid robot in history just went on sale. Unitree’s G1 lists at 13,500 dollars, less than a used sedan, and the internet promptly decided the robots had arrived. The price is real. The conclusion is wrong.

Here is the catch the sticker hides. That 13,500 dollar model explicitly does not support development. The version you can actually build on, the EDU grade, starts around 44,000 dollars. Add dexterous hands, tactile sensors, site integration, safety cages and the data labelling needed to teach it your specific task, and a single deployed unit lands closer to 110,000 dollars. Buying the hardware is not buying a worker. The robot is the cheap part.

Now the part that keeps this honest, because it cuts the other way too. Even at a fully loaded cost of roughly 14.60 dollars per productive hour on a single shift, a humanoid still undercuts human logistics labour, which runs from about 24.60 dollars an hour in retail to 49 dollars an hour in warehousing. So this is not a hype takedown. In a structured warehouse, the economics already work. The value just does not come from a cheap robot. It comes from swapping high-turnover human labour for a predictable, depreciating asset.

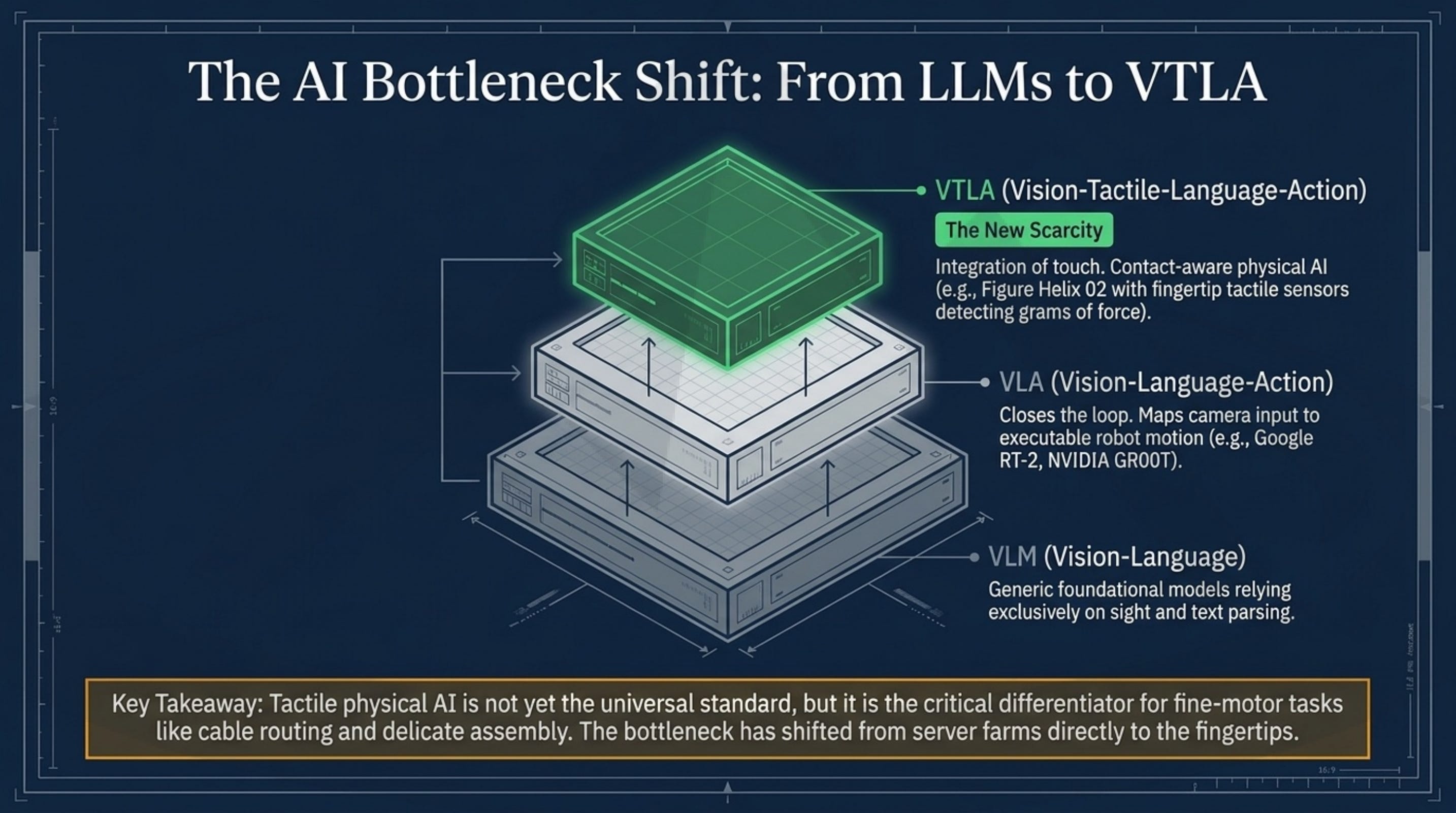

So if the robot is not the scarce thing, what is. For a decade the binding constraint in AI was compute. Large language models handed us a surplus of digital thinking. What is scarce now is physical doing, the ability to touch, grip and act reliably in a messy room. The bottleneck moved from the server farm to the fingertips.

Once you see it that way, the scarcity shows up in three places, and none of them is the robot. First, data. By industry estimates there are only around 300,000 hours of high-quality physical-manipulation data in the entire world, and under 5,000 of them are open-source. The moat accrues to whoever owns the proprietary telemetry coming off real factory floors, not to whoever sells the shell. Second, components. The muscles that decide whether a robot is a toy or a worker, the precision roller screws and the high-efficiency magnets, are made by a tiny handful of firms. That is a genuine chokepoint. Third, geopolitics. Since April 2025 China has required export licences for the rare earths, terbium and dysprosium, that go into humanoid motors, while pouring state money into its own robot supply chain. This is a supply war, not just a technology race.

And the reality check most of the excitement skips. The sector has reached regular productive use. Figure’s robots met an 84-second cycle on a BMW line at better than 99 percent accuracy. Agility’s Digit has moved more than 100,000 totes for a logistics customer, and the company is going public through a 2.5 billion dollar deal, the first Western pure-play to try it. All real. But nobody has yet reached large-scale repeat orders with disclosed, positive unit economics. The most expensive fact in the entire theme is that the highest valuations sit on the companies with the least visible humanoid revenue.

We took the whole thing apart in a new deep dive, “The Humanoid Bottleneck: Physical AI and the New Scarcity.” Nineteen pages: the value chain split into muscle and brain, the specific component chokepoints, the data moat, three scenarios for 2030, and where in this chain the scarcity actually gets paid. It is the desk’s work, and it is at moatpeak.com.

Educational research only. Not investment advice. MB “MoatPeak Group”.