A blowout earnings report just got a shrug. The reason isn't the company.

One of the best quarters in a chipmaker's history barely moved the market. What good news is worth depends on what interest rates are doing.

Yesterday, one of the world’s big memory-chip makers reported a quarter that, on paper, was about as good as they come. Revenue several times what it was a year earlier, the highest profit margins in the company’s history, guidance raised, and its AI memory effectively sold out. The kind of report that in a different year sends a stock to the moon and tows the whole market up behind it. This time the shares popped after hours and the broad market basically shrugged. Same blowout, very different welcome — and the reason has almost nothing to do with the company.

What changed was the weather around it. In the same few days, the market quietly stopped expecting interest-rate cuts and started pricing the opposite: a real chance of hikes. You could see it in an odd place. Gold, which had climbed all year, broke below $4,000 for the first time in months. When a historic earnings beat and a gold breakdown show up in the same week, the thread tying them together isn’t earnings or gold. It’s rates.

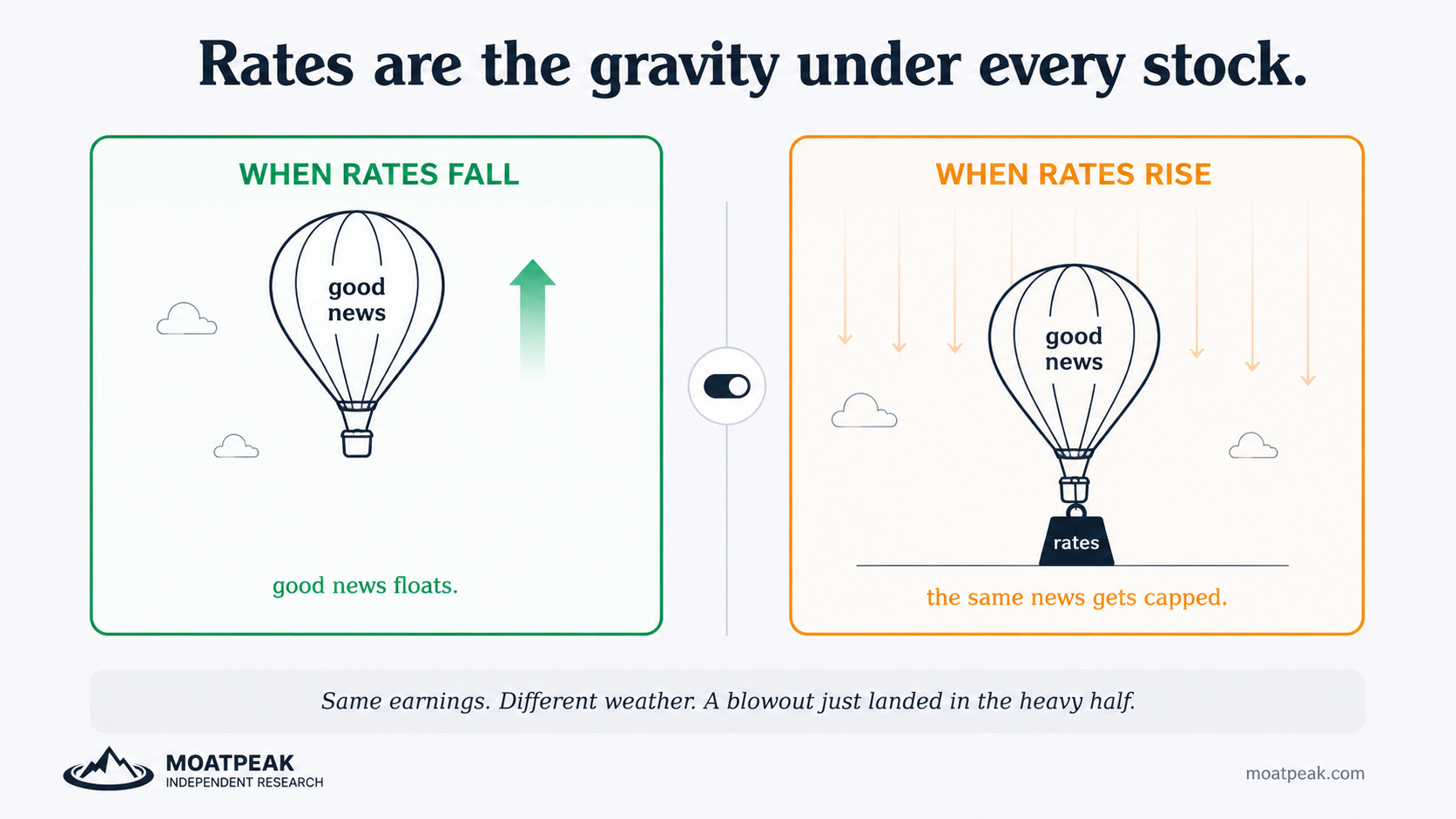

Here’s the part worth keeping. A stock is, in the end, a claim on the cash a company will throw off in the future. To value it, you shrink that future cash back to what it’s worth today, and the size of that shrink is set by interest rates. When rates fall, future cash is worth more now, so good news gets amplified and every beat echoes louder. When rates rise, the same future cash is worth less, so even great news gets a ceiling quietly lowered onto it. Investors sometimes call interest rates the gravity behind asset prices, and it’s a good way to picture it. Low gravity, things float higher on less. High gravity, even strong news struggles to get off the ground.

So the muted reaction wasn’t really a verdict on the chipmaker. The company did its job. It’s that the report landed in heavier gravity than the one investors had grown used to. Under a Fed the market expected to cut, those record margins would have lit a melt-up. Under a Fed it now thinks might hike, the same margins are a reason to own a cash machine and little more, because the discount working against every valuation just got bigger instead of smaller.

The useful takeaway isn’t about one chip stock or one metal. It’s that you can’t read an earnings report in a vacuum, because the same numbers are worth different amounts in different rate weather. And it tells you where the strain lands hardest. Gravity barely troubles a business already producing a lot of cash today. It’s punishing on the expensive, profit-light “story” stocks priced almost entirely on cash that’s years away — the exact names that floated highest when gravity was low. When the weather turns, those feel it first.

We wrote not long ago that the market’s old comfort — the assumption that cheaper money is always just around the corner — was being quietly folded away. This week looked like the market starting to believe it, and repricing the trades built on the opposite. None of this is a call on that chipmaker, on gold, or on the Fed’s next move. It’s a lens: before you decide a great quarter is a great investment, check what the weather is doing to it. What we think that means for positioning is the desk’s work at moatpeak.com.

Free weekly letter and explainers like this; the daily research, levels and the Daily Compass are at moatpeak.com.

Educational research only — not investment advice. MoatPeak Group, UAB.