A delayed IPO just knocked 12% off one of the world's biggest investors

How the eye-watering valuations of private AI companies quietly depend on a stock-market exit that hasn't happened yet.

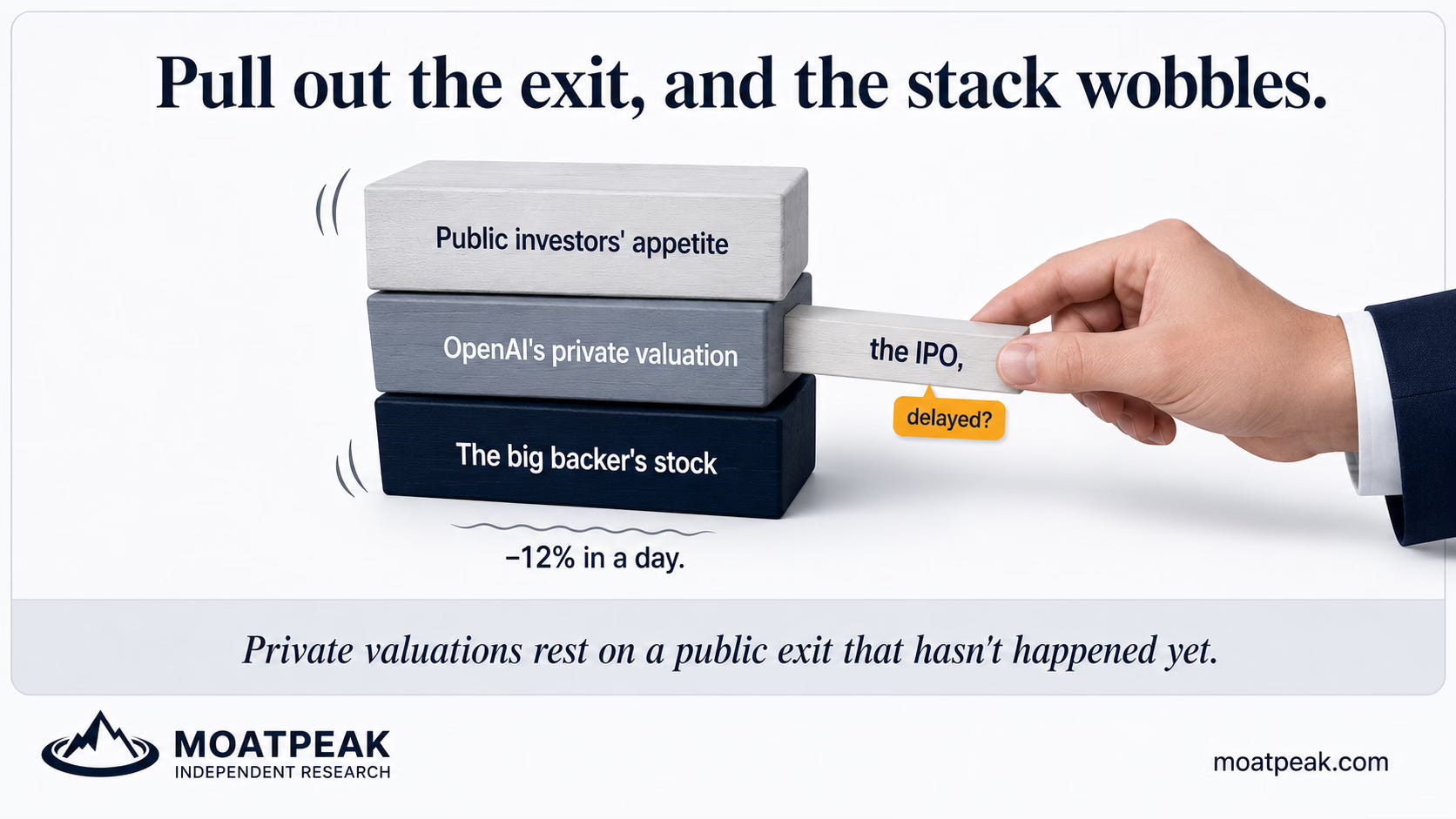

One of the world’s largest tech investors lost more than a tenth of its value in a single day last week. There was no bad earnings report, no scandal, no failed product. The trigger was a news story suggesting that OpenAI, which the firm has poured tens of billions into, might wait until 2027 to go public rather than list sooner. A delay. Not a cancellation, not a write-down, just a maybe-later. And the market took 12% off the company on the spot.

To see why a delay does that much damage, follow how money actually gets made in private companies. When a firm invests billions in a startup, that stake is worth something only on paper until there’s an exit, usually an IPO, where the public market finally puts a real, tradable price on it. The whole structure of private valuations leans on the expectation of that future payday. Push the payday further out, or make it less certain, and every number underneath it has to be marked down a little, today.

Now stack the layers up. The big investor’s record valuation rested heavily on the promise of cashing out of OpenAI at an enormous price one day. OpenAI’s own valuation rests on the promise that public investors will eventually pay up for it. And the appetite of those public investors rests on how the last few big tech listings have gone, which lately has been bumpy. It’s a tower of promises, each block balanced on the one beneath it actually coming true. Last week one block wobbled, and you could watch the shake travel all the way down.

You might think none of this touches you if you don’t own the names involved. But the same logic sits under a lot of what you do own. Plenty of ordinary public companies carry a price that assumes some big future event lands on schedule: a product launch, a drug approval, a payoff a few years out. When the market is relaxed it pays for those promises in advance. When it gets nervous it stops fronting the money and demands to see the thing first. The lesson from last week isn’t really about one investor. It’s about how fast “priced for a sure thing” can flip to “show me.”

So when you look at something you hold, it’s worth asking what’s already baked into the price. Is it valued for what it earns now, or for a happy ending that hasn’t arrived yet? Neither is wrong, but the two behave very differently when the mood turns. The names priced for the happy ending fall hardest on nothing more than a delay, because a delay strikes at the one thing holding them up, which is the timing of the payoff. Knowing which of your holdings are running on promises, and how patient those promises need you to be, is the kind of work we do on the desk at moatpeak.com.

*Free weekly letter and explainers like this; the daily research, levels and the Daily Compass are at moatpeak.com.*

*Educational research only — not investment advice. MoatPeak Group, UAB.*