A green week, under a new ceiling

Stocks rose last week — but a hawkish new Fed quietly capped how far valuations can stretch, and part of the calm was borrowed from a fragile oil truce. The week in one read.

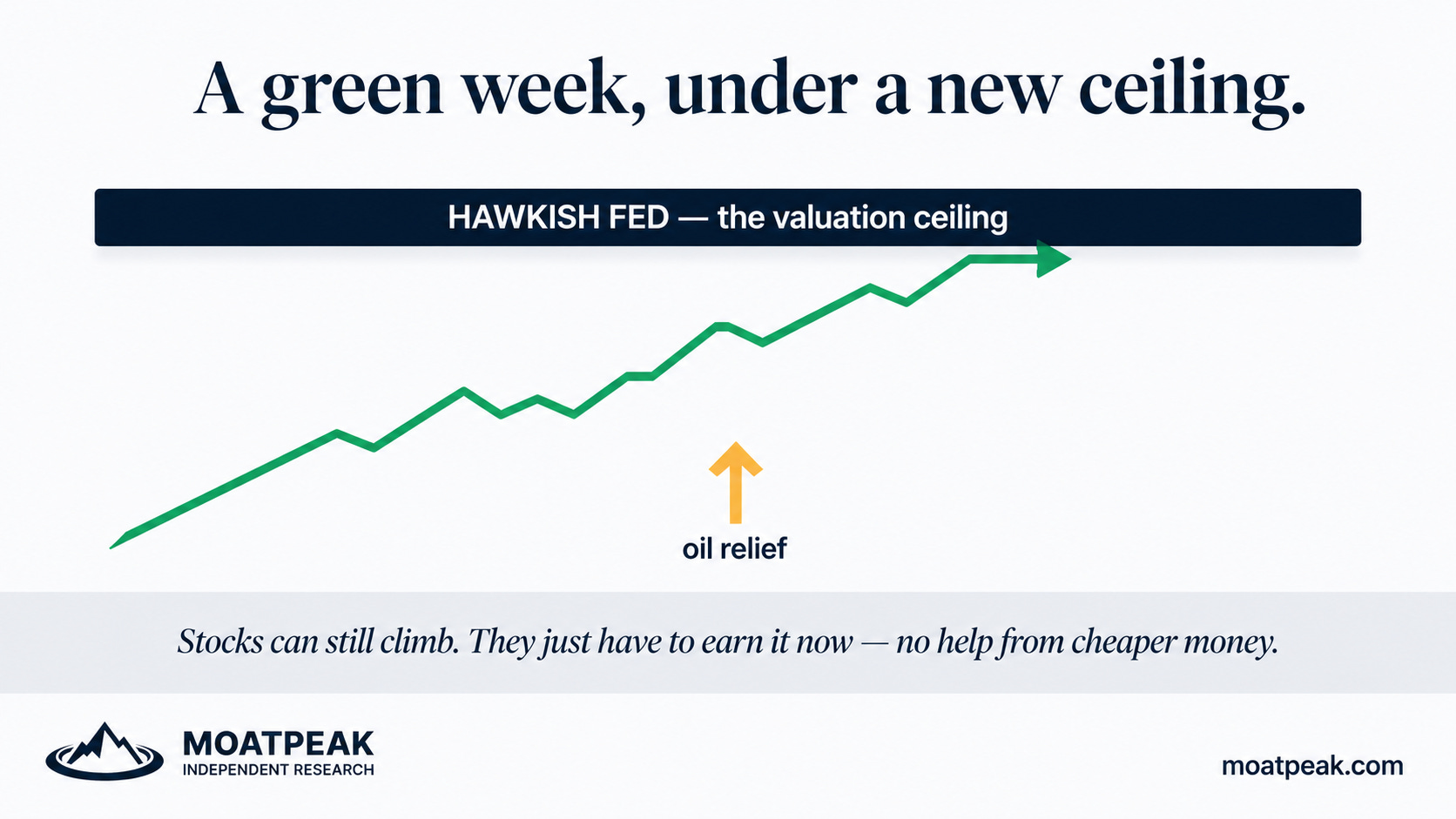

On the screen, last week looked like a quiet win. The S&P drifted up toward fresh highs, the headlines were calm, and most people filed it under “more of the same.” Underneath, the character of the market changed in a way worth a few minutes of your time. Two forces pulled in opposite directions all week, and where they settled tells you more than the index level did.

The first force was relief. A tentative framework to wind down the conflict with Iran, brokered out of Islamabad, sent crude tumbling — down roughly a fifth from its highs for the year — as the Strait of Hormuz looked set to reopen. Cheaper energy is the kind of thing that lifts the mood: lower input costs, softer headline inflation, a reason to buy. For a few sessions it did exactly that.

The second force was heavier, and it’s the one that lingers. The Fed held its first meeting under a new chair, and the tone was firmly hawkish: officials nudged up their own rate projections and, tellingly, dropped the soft forward guidance markets had leaned on for years. The message under the message was that this Fed cares more about pinning down inflation than about keeping the market comfortable. (We dug into that shift — a Fed that’s stepped back from telling you its next move — in a recent note.)

Put the two together and you get the week’s real story. Stocks can still rise, but the new Fed has quietly lowered a ceiling over how far valuations can stretch. For years a big chunk of returns came not from companies earning more, but from investors happily paying more for each dollar of those earnings — and that willingness ran on the expectation of ever-cheaper money. A hawkish Fed takes that lever away. From here, gains have to be earned the hard way, through real profit growth, rather than borrowed from a friendlier discount rate. That’s the ceiling. The index can keep climbing under it; it just has to do more of the work itself. (It’s the same gravity we explored in a recent Decoded piece: when rates rise, every dollar of future profit is worth a little less today.)

You could see the new regime in the week’s sharpest moves. One of the world’s largest consulting firms reported a perfectly good quarter and lost nearly a fifth of its value in a day, because the market stopped paying for the story and started pricing the threat underneath it. The dollar pushed to its highest in a year, which quietly tightens conditions everywhere and means a slice of any “record” is really just the measuring stick moving — gold slipped even as stocks held. None of these were one-offs. They’re what a market under a ceiling looks like.

And the cheerful half of the week sits on a shaky leg. The oil relief depends on a truce that, by every account, is preliminary and fragile — a pause, not a settlement. So part of last week’s calm is borrowed, and worth holding loosely. When a market quietly un-prices a live risk, it doesn’t become safer; it just becomes cheaper to be caught out by.

So the useful way to read a week like that isn’t “stocks up, all clear.” It’s that the engine changed. Cheaper money is no longer the wind at your back, the easy gains from rising multiples have a lid on them, and some of the calm is on loan from a fragile truce. None of that is a reason to panic. It’s a reason to value businesses on what they actually earn, and to notice when the index’s strength is the real thing versus the borrowed kind. The week’s specifics — the levels, the odds, and what we’re actually doing about them — are the desk’s work at moatpeak.com. The shape of the week is the part worth carrying into this one.

Free weekly letter and explainers like this; the daily research, levels and the Daily Compass are at moatpeak.com.

Educational research only — not investment advice. MoatPeak Group, UAB.