Accenture had a good quarter. The stock fell 18% anyway.

Earnings were up. Margins were up. Cash was pouring in. It was still the worst day in the company's history.

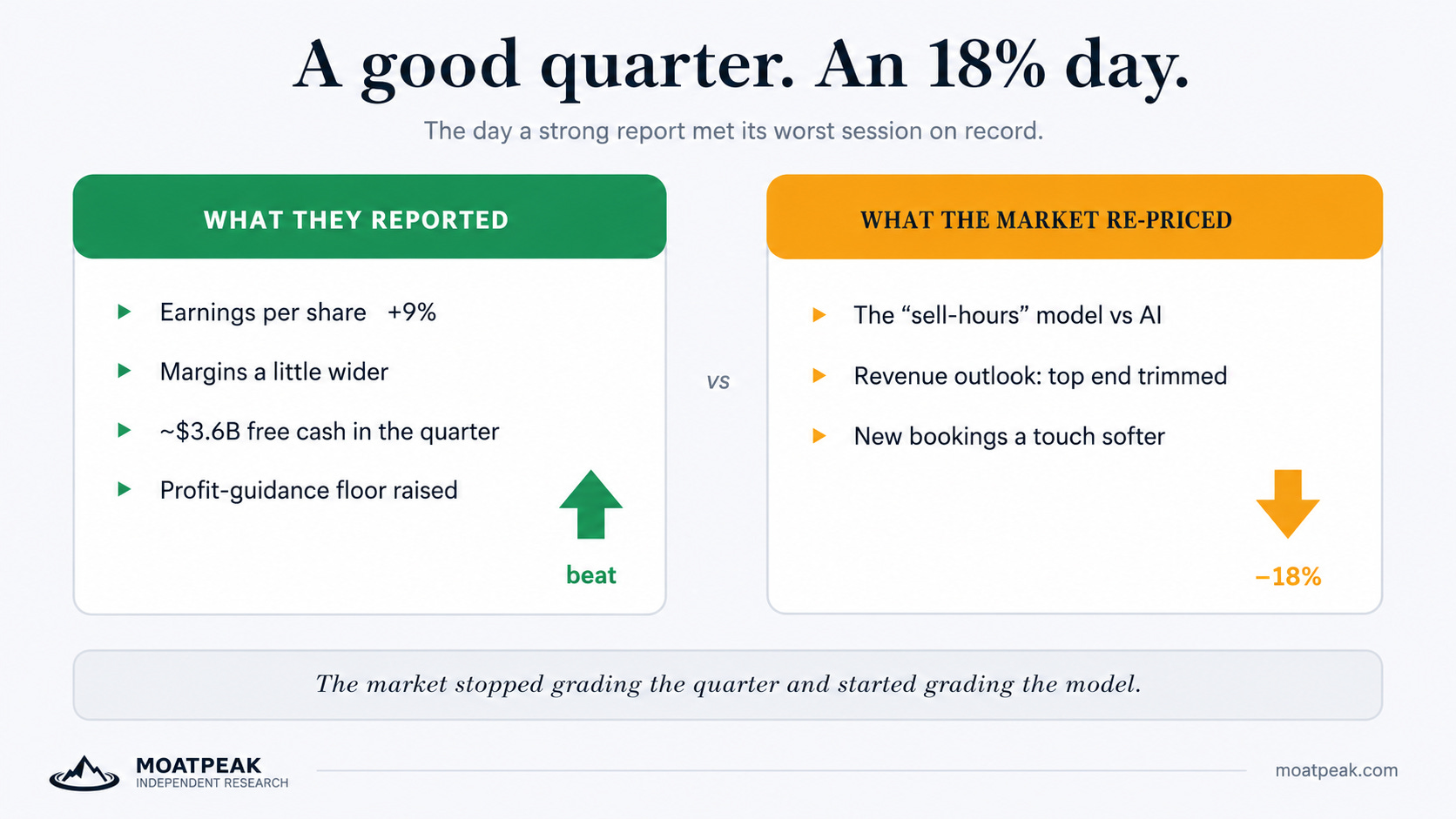

This week one of the biggest consulting firms in the world told investors it had made more money than expected. Earnings per share up around 9%. Margins a little wider. About three and a half billion dollars of free cash in a single quarter, and management actually raised the floor on its profit forecast for the year. The stock fell almost 18% that day, the worst single session in the company’s history. Both were true on the same afternoon.

The reflex most of us learn early is that a company beats expectations and the stock goes up. So when a beat gets answered with a near-record sell-off, the natural guess is that something in the numbers was quietly rotten. It mostly wasn’t. The quarter was solid. What broke was the story investors are willing to tell about the next several years.

Two less flashy details did the work. The firm shaved the top end off its revenue growth outlook, and new bookings, the future work clients commit to now, came in a touch below last year. Neither is a catastrophe on its own. But they landed on a question that’s been following the whole industry around: what happens to a business that sells hours of human expertise once AI starts doing a chunk of those hours for free?

That’s the part worth slowing down on. Investors weren’t really arguing about the last three months. The selling was aimed at the engine underneath, the “pay us for our people’s time” model these firms are built on, because that engine now has a believable threat pointed at it. Once the worry shifts from “how was the quarter” to “does the model still hold,” one good quarter can’t keep the stock up by itself.

For a normal investor the useful bit isn’t about this one company. It’s that a share price runs on two different clocks. There’s the fast one, did they hit this quarter’s number, and the slow one, is this still a good business a decade from now. Most of the time the two move together and you’d never know they were separate. Every so often a single day yanks them apart, and you get a strong quarter sitting right next to a falling stock. When that happens, the move is usually the slow clock changing its mind.

None of this settles whether the fear is correct. Maybe AI hollows out the sell-hours model. Maybe these same firms end up selling the AI itself and come out the other side bigger than before. That argument is far from over. What this week made clear is smaller and more practical: a good quarter and a sinking share price can show up in the same breath, and when they do, it’s worth asking which clock the market just re-read. Where we think that leaves the sector, and what we’re doing about it, is the desk’s work at moatpeak.com.

Free weekly letter and explainers like this; the daily research, levels and the Daily Compass are at moatpeak.com.

Educational research only — not investment advice. MoatPeak Group, UAB.