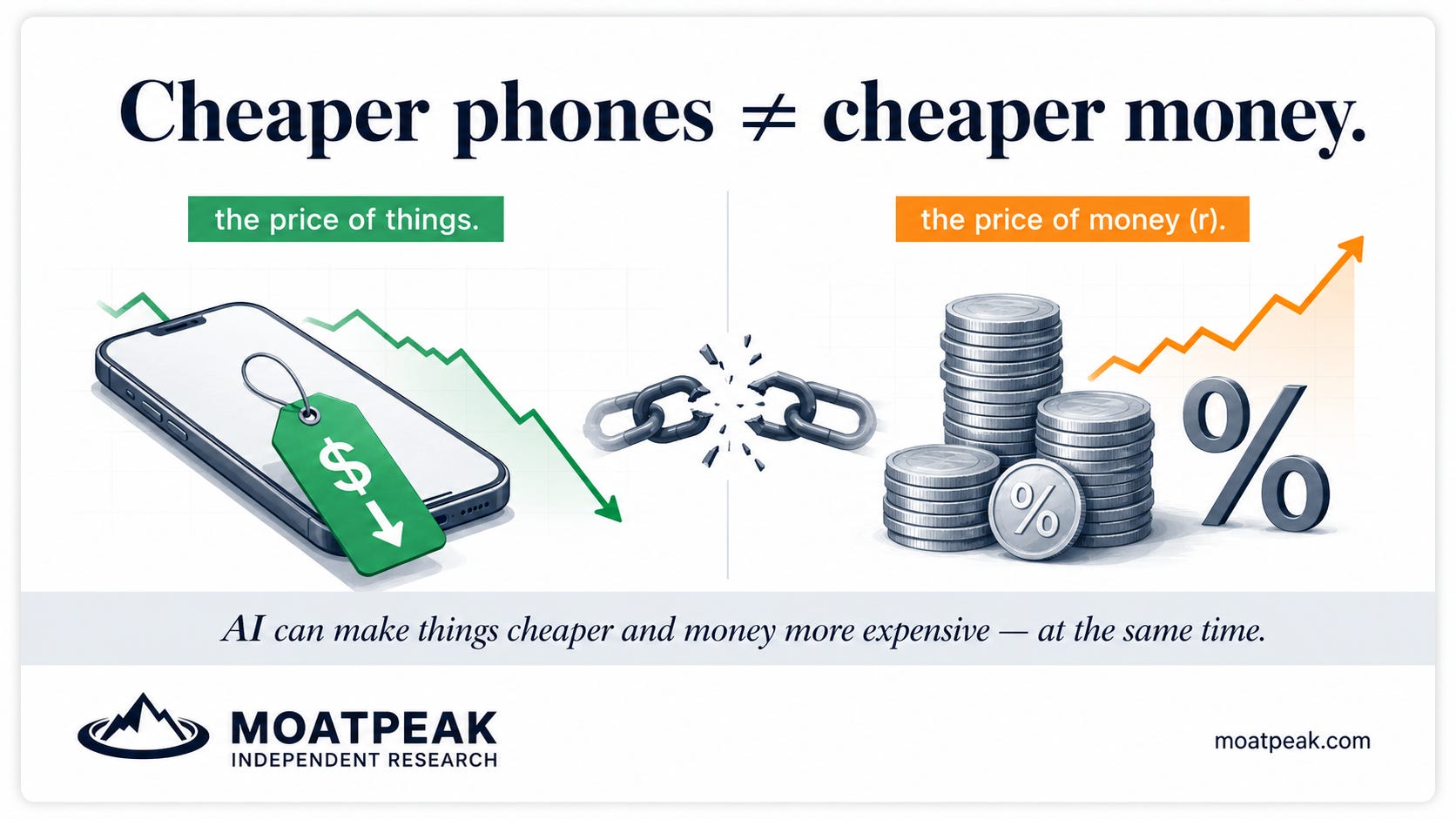

Cheaper phones don't mean cheaper money.

"AI makes everything cheaper, so interest rates will fall" sounds airtight. The last step is probably wrong — and seeing why is a genuinely useful piece of financial literacy.

Here is a chain of reasoning that sounds completely airtight, and that a lot of genuinely smart investors quietly believe. AI makes companies more efficient. Efficiency pushes prices down. Lower prices mean lower inflation. So interest rates will fall. Four steps, and each one feels obvious as you read it — the kind of logic that’s comfortable to hold and easy to nod along to. It’s also probably wrong, right at the very last step. And seeing why it’s wrong is worth more than the conclusion itself, because it teaches a habit you can reuse forever.

Start with what actually sets interest rates over the long run. Beneath all the day-to-day drama of central-bank meetings, rates are tugged toward something economists call the neutral rate — nicknamed “r-star.” It’s the rate of interest that neither speeds the economy up nor slows it down: the economy’s natural resting pulse. And crucially, that resting pulse isn’t set by inflation alone. It’s set mostly by two deeper things — how productive the economy is, and how hungry for investment capital it is. That second ingredient is exactly where the popular four-step logic quietly falls apart.

Because if AI genuinely delivers what its champions promise — if it really does make workers and machines dramatically more productive — then the rational response from businesses is not to sit still and enjoy lower costs. It’s to invest more. Build more data centres. Retool more factories. Chase the higher returns that new productivity suddenly makes possible. And when everyone wants to borrow and build at once, the price of capital — which is to say, the interest rate — gets pushed up, not down. A real productivity boom is one of the classic ways the neutral rate rises. Which means the very same AI revolution that makes your gadgets cheaper could quietly make money itself more expensive.

The trap here is a specific one, and naming it is the whole point, because you’ll meet it again and again: it confuses “some things get cheaper” with “the price of money falls.” Those are two entirely different prices, set by different forces. The cost of a television and the cost of borrowing for ten years have almost nothing to do with each other. AI can comfortably push the first one down while pushing the second one up — both at the same time. The seductive chain quietly assumes the two must move together, and they simply don’t have to.

There’s a broader habit of mind buried in all this, and it’s the real souvenir to take home. Be most suspicious of the investment logic in which every single link sounds obvious. If a chain of reasoning is that smooth, that satisfying, and that widely believed, the market has almost certainly already priced it — which means the money is made or lost on the one link everybody glossed over. Here, that overlooked link is r-star. The obvious part (AI makes gadgets cheaper) may well be perfectly true. It’s the conclusion everyone confidently bolted onto the end — and so rates will fall — where the thinking quietly went slack.

Cheaper phones don’t mean cheaper money. And whenever a piece of market logic feels too smooth to argue with, the genuinely interesting question is always the same: which step did we wave through simply because it felt obvious?

Free weekly letter and explainers like this; the daily research, levels and the Daily Compass are at moatpeak.com.

Educational research only — not investment advice. MoatPeak Group, UAB.