Everyone is watching the wrong screen

The stock market fell hard today, and every headline will tell you why. The useful signal was somewhere almost nobody is looking: the market that did not crash.

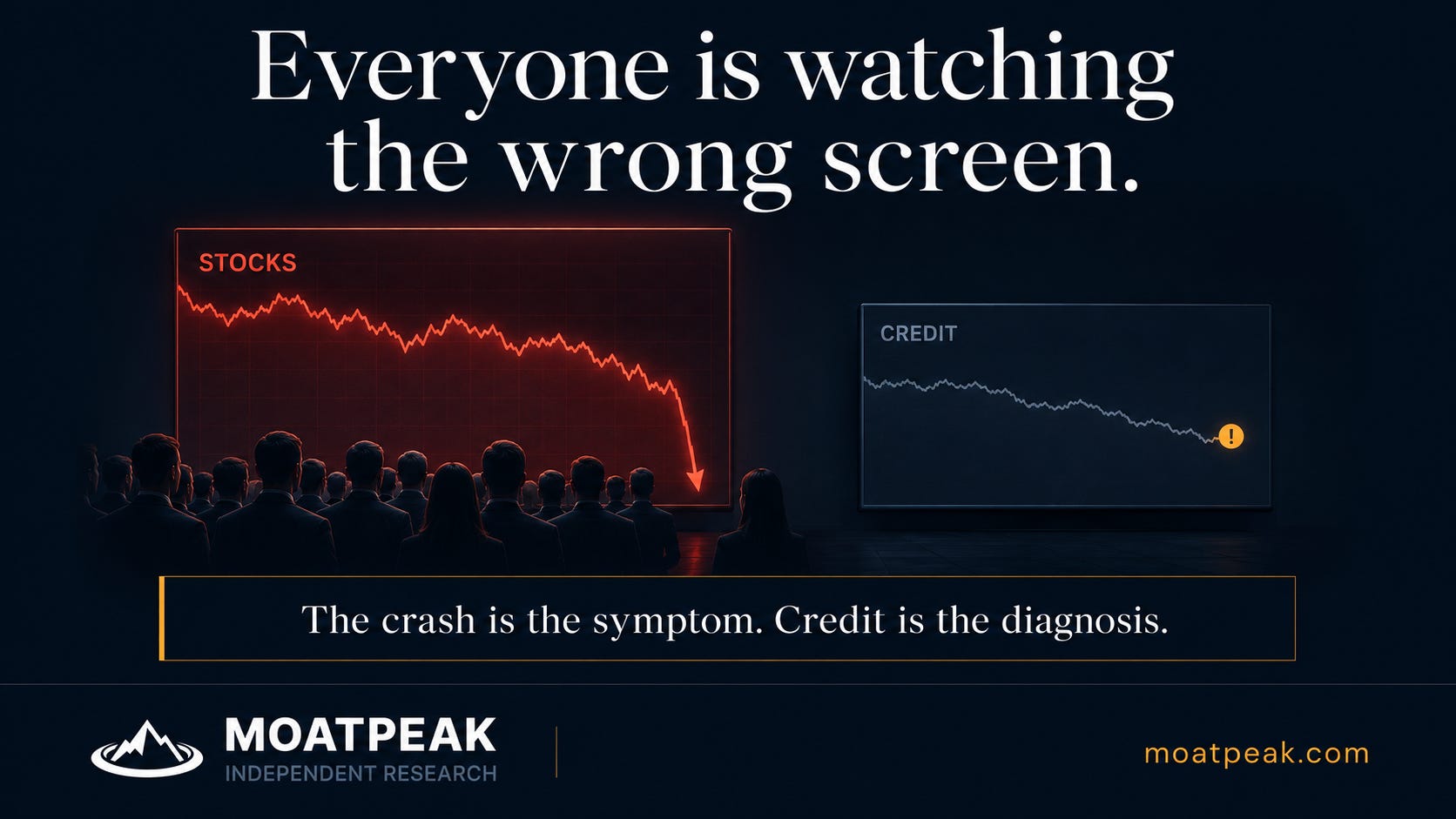

Today the screens are red and the story writes itself. Korea’s main index fell 8 percent overnight, tripping a circuit breaker that halted trading outright. Oil jumped as the Strait of Hormuz was declared closed again. Every headline you will read today is a version of the same sentence: stocks fell because of Iran. That sentence is true, and it is also close to the least useful thing you can know right now. The real signal today was not in the market that crashed. It was in the market that did not.

Here is the part almost nobody is pointing at. While equities took the dramatic 8 percent air-pocket, the bond market did something quieter and far more telling. For the first time in a long time, the corner of the market that trades company debt looked more rattled than the stock market did. On a day the S&P barely moved, the price of insuring and owning corporate credit was deteriorating at a pace you usually only see when something is actually breaking. That is a role reversal, and it matters because of an old and reliable rule: equity ignores almost everything happening in credit, right up until the moment it suddenly notices. Stocks are the loud market. Credit is the smart one. When the two disagree about how worried to be, the bond market is usually the one worth believing.

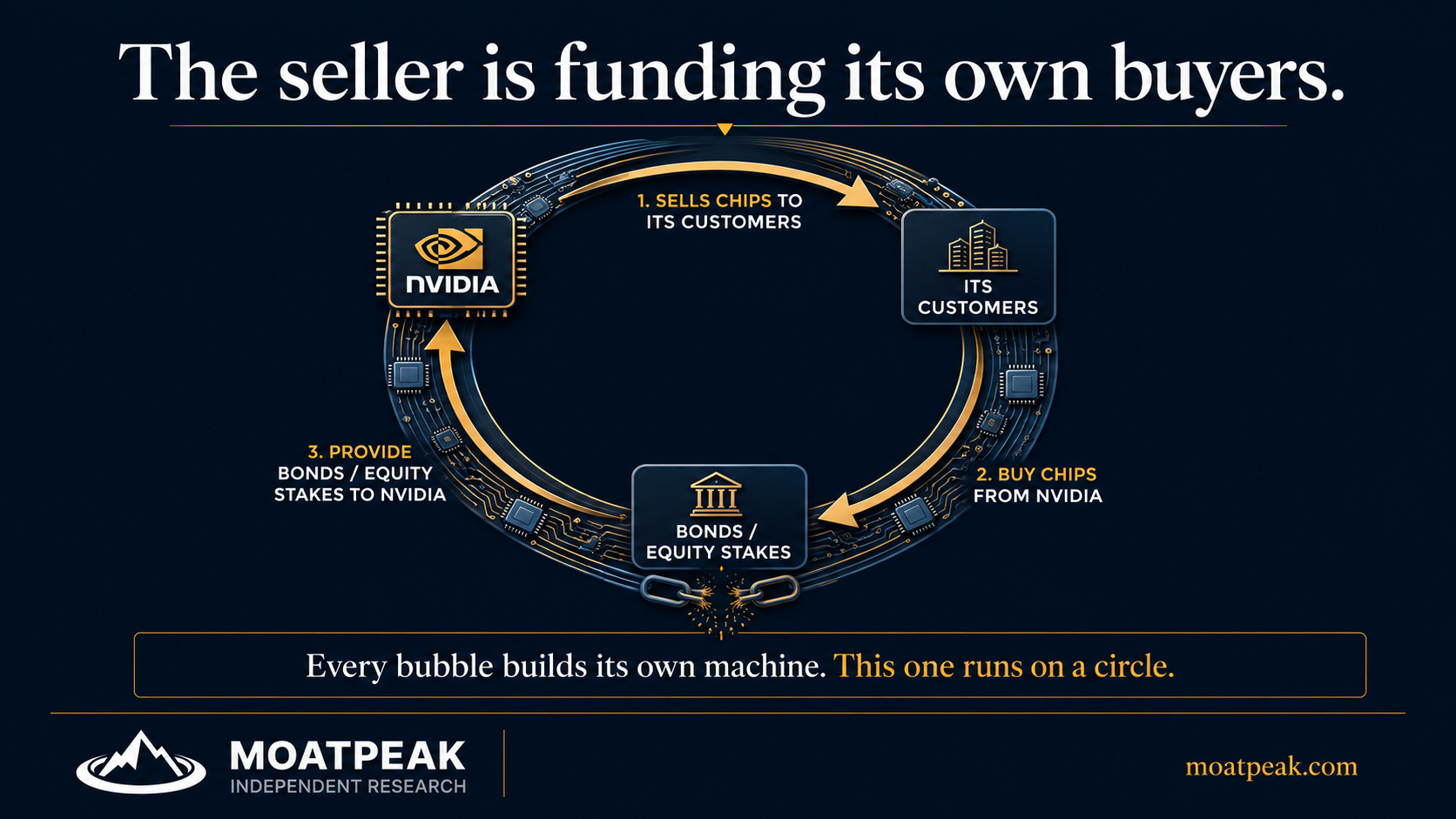

So why is credit the nervous one this time? Because of what has quietly been paying for the entire AI boom. For most of this cycle, the buildout was funded by profits and stock. In a matter of months it has become a debt story. A small cluster of AI giants has issued around 182 billion dollars of bonds this year, up roughly thirteen hundred percent from a year ago, and now accounts for close to a sixth of the entire US investment-grade bond market by itself. That alone would be worth watching. But the part that should make you sit up is not the size of the money. It is the shape of it. The money has started to move in a circle.

Nvidia, the company selling the chips, has been investing tens of billions of dollars into the companies that then turn around and buy its chips. It has committed to funding OpenAI, whose own finance chief has openly acknowledged that most of that money will flow straight back to Nvidia. It holds stakes in cloud providers that pledge Nvidia chips as collateral to borrow money, in order to buy more Nvidia chips. Read that twice. The seller is financing its own buyers. A meaningful slice of what looks like independent demand is, in part, the supplier writing checks to itself. This has a name. It is called vendor financing, and the last time it defined a boom was the telecom bubble of the late 1990s, when roughly a fifth of one famous equipment maker’s revenue was effectively money it had lent to its own customers. That did not end the technology. It did end the prices.

This is why we keep saying that every bubble builds its own machine. The railroads had land grants. The dot-com boom had venture capital. Housing had subprime lending. This AI cycle increasingly has this loop of chips, equity stakes and bonds. And the uncomfortable thing about a machine like that is that it runs in both directions. On the way up it manufactures its own demand and its own confidence. On the way down, the very same links that amplified the boom transmit the stress, from a customer, to the debt secured against it, to the supplier who quietly funded both. That is precisely the kind of chain a credit desk is paid to watch, and precisely the kind a stock index is the last to price.

There is one more piece, and it is the one that turns a wobble into a real risk. Going into this weekend, the market was priced for nothing to happen. Volatility sat near its lows, the degree to which stocks move together had fallen to a record low, and the options market was charging almost nothing to protect against a shock. That looks like calm. It is closer to the opposite. A market where everyone has quietly unclipped their seatbelt because the road has been smooth is not a safe market. It is a fragile one, because there is nothing left to absorb the first real bump. The time to buy an umbrella is when the sky is blue and umbrellas are cheap, not in the first minute of the downpour when everyone reaches for one at once.

So here is the useful way to hold today, and it is almost the mirror image of the panic on the screens. The 8 percent equity drop is the symptom, and symptoms are loud. The price the bond market is quietly putting on all that AI debt is the diagnosis, and diagnoses are quiet. Whether this is a passing air-pocket that gets bought back or the first crack of something larger will not be settled by the index everyone is staring at. It will be settled in the corner of the market almost no one is watching. We are not here to tell you to buy the fear or to sell it. We are here to tell you where to point your eyes. Watch the market that is not crashing.

On our own daily read, this is the kind of break that changes how defensive we think it is worth being, and the discipline is to move when the tell breaks rather than when the headline lands. Where we would actually lean from here, and the single spread we are watching to tell a buyable wash-out from something worse, is the desk’s job at moatpeak.com.

The free work is where we show you where to look. The daily reading and the levels are the desk’s job at moatpeak.com.

Educational research only. Not investment advice. MoatPeak Group, UAB.