Gold isn't a bet on getting rich. It's a message about everything else.

Several major banks now expect gold meaningfully higher. The interesting part isn't the number — it's what it says they're worried about.

Gold has been on a tear — fresh highs, and several of the biggest banks on Wall Street now openly expect it meaningfully higher still, with year-end targets that would have sounded slightly unhinged a couple of years ago. That’s worth noticing, but the number itself isn’t the interesting part. The interesting part is what a rising gold price is actually telling you — because gold is a genuinely strange asset, and learning to read it is a quietly useful skill.

Here’s the strangeness. A share of a company earns money. A bond pays interest. A flat collects rent. Gold does none of that. It sits in a vault and looks exactly the same in a hundred years. No earnings, no dividend, no management, no product, no growth. By every yardstick we normally use to value things, gold should be inert and going nowhere. So when it climbs, and climbs hard, it cannot be because “the business got better” — there is no business. Something else entirely is being priced. And that something else is the whole point.

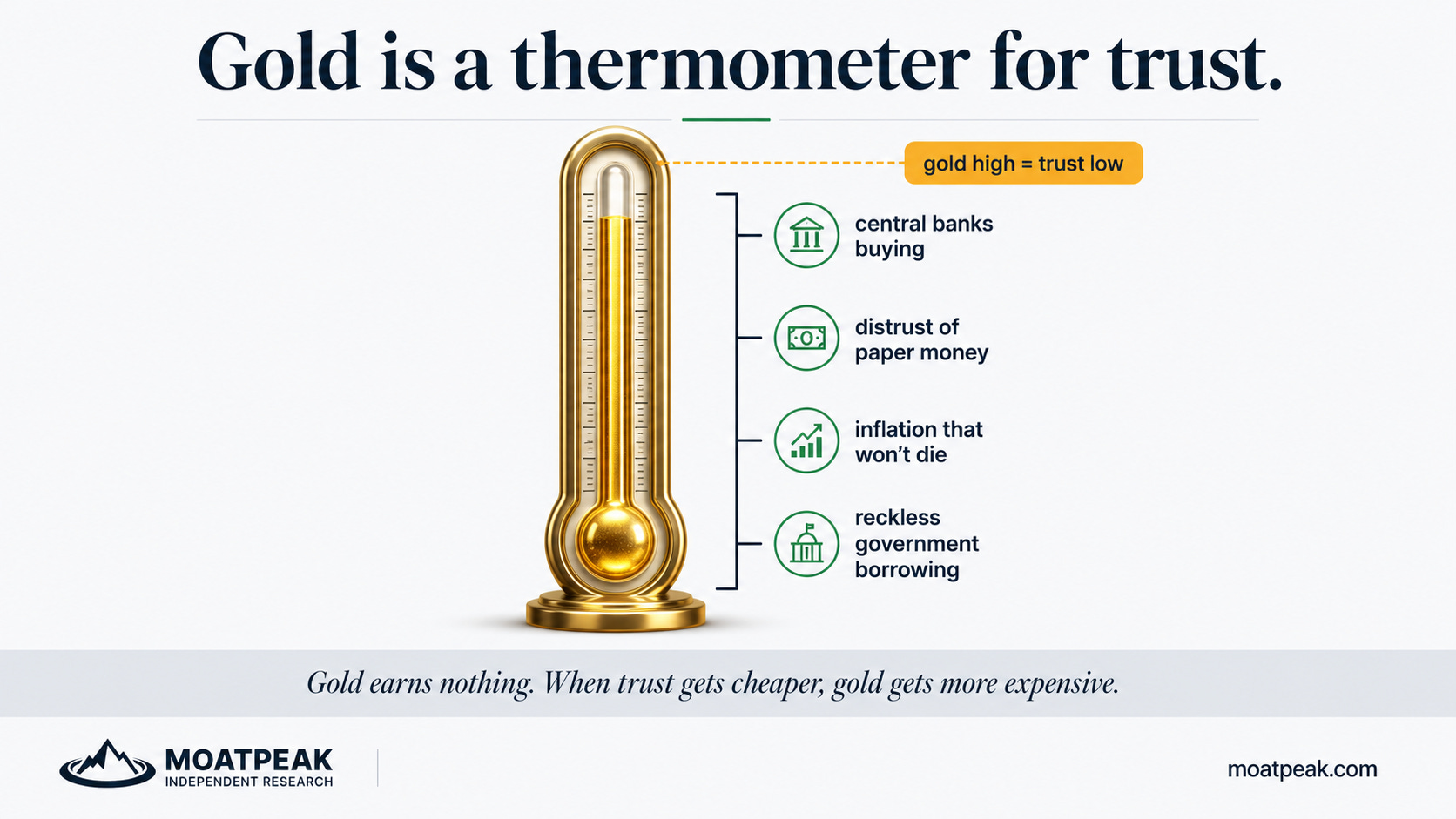

Gold is best understood not as an investment in something, but as insurance against a few specific things. It’s what people reach for when they start to distrust paper money: when governments borrow without any visible plan to stop, when inflation runs warm for years and quietly eats savings, when the promise behind a currency feels a shade less solid than it used to. A rising gold price is the cost of that insurance going up. It usually means that, collectively, the world is deciding it wants more protection against disorder — against debts that look unpayable, against money that keeps buying less, against the nagging worry that whoever controls the printing press won’t put it down. Gold doesn’t shout. It just gets more expensive when trust gets cheaper.

And here’s the detail that turns this from a nice theory into something concrete. The biggest buyers of gold lately aren’t nervous individuals hoarding coins — they’re central banks, the very institutions that print the paper money. All over the world, they’ve been quietly swapping some of their dollars for gold, month after month. Sit with that for a second: the organisations that manufacture currency are themselves buying the one thing they cannot manufacture. When the house starts hedging against its own chips, it’s worth asking what game the house thinks it’s in.

So what do you do with this? Nothing dramatic — and to be completely clear, nothing this piece is telling you to buy or avoid. Gold is volatile, it pays you precisely nothing to hold it, and it can fall hard too; plenty of people have been burned chasing it. The value here isn’t a trade, it’s a translation. Next time you see “gold hits record” flash past, don’t file it under “shiny thing goes up.” File it under “the world is paying more for protection against the things that keep grown-ups awake at night.” Gold is a thermometer for trust — in money, in governments, in the whole system holding it together. And it’s worth knowing how to read a thermometer, even if you never intend to hold one.

Free weekly letter and explainers like this; the daily research, levels and the Daily Compass are at moatpeak.com.

Educational research only — not investment advice. MoatPeak Group, UAB.