In a gold rush, sell shovels: who actually keeps the AI money

Monday looked like the AI trade cracking. Underneath, the market was quietly sorting the firms that pay for AI from the ones that get paid for it.

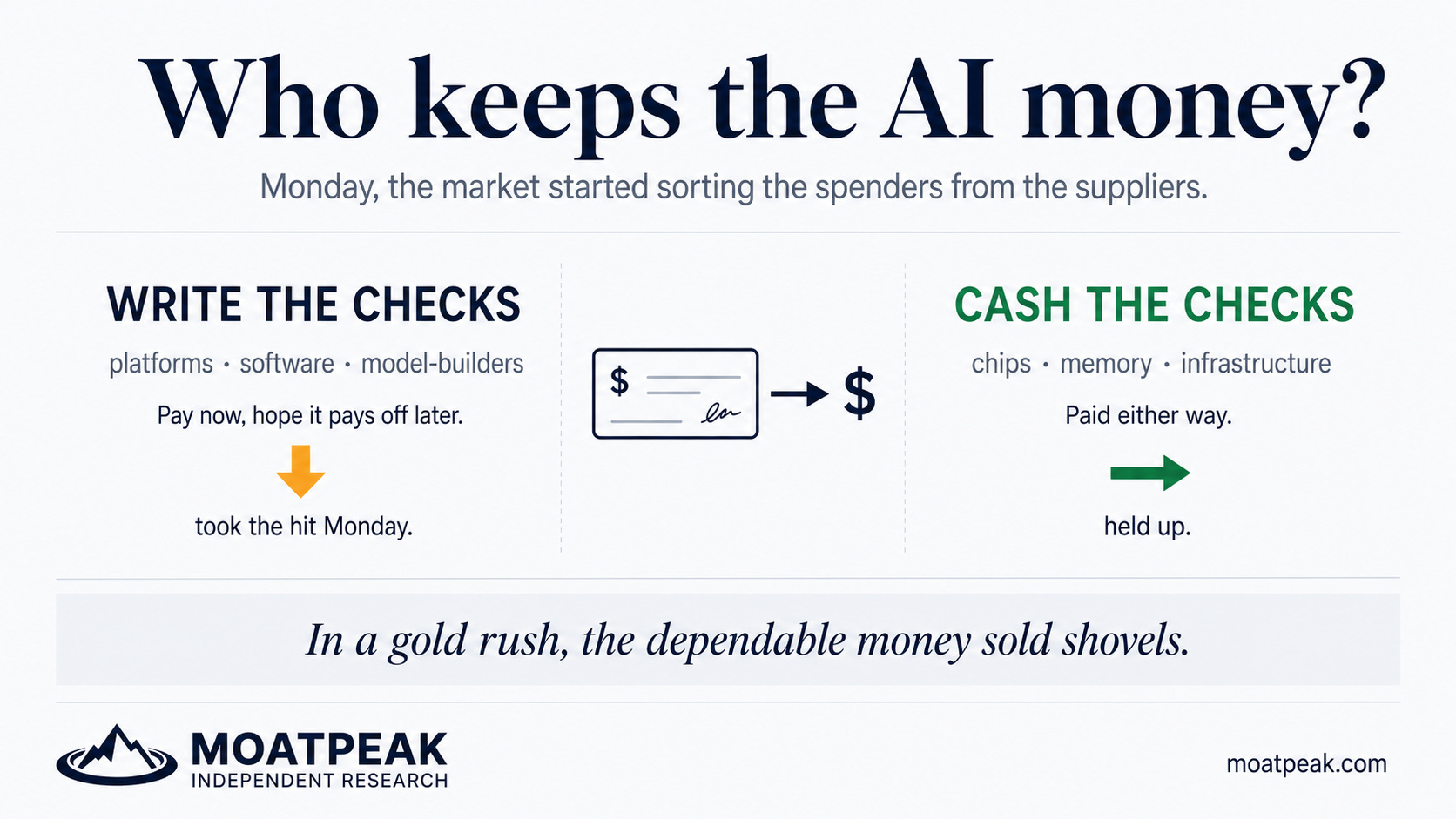

On Monday the headlines said the AI trade was finally cracking. The most-owned space name fell around 16% in a day, the big platforms slid, and the press reached for the word “bubble.” Look one layer down, though, and it wasn’t really AI getting sold. It was a sorting.

Roughly speaking, the market split the AI world into two piles. In one, the companies writing the big cheques: the platforms and software houses pouring fortunes into chips, data centres and models, on the bet it pays off down the line. In the other, the companies cashing those cheques: the firms supplying the picks and shovels, who get paid now whether or not the bet works. On Monday the cheque-writers took the hit. A lot of the cheque-receivers held up, or rose.

This is an old pattern in new clothes. In the actual gold rush, plenty of miners went home with empty pockets while the people selling them shovels, jeans and train tickets did fine either way. The dependable money sat with whoever got paid regardless of whether the gold turned up. Every capex boom since has rhymed with it. Monday didn’t downgrade AI; it downgraded one side of it — the side doing the spending.

Two things make the cheque-writers’ side trickier than a revenue chart lets on. The first is that the gear they’re buying ages fast. When a company spends billions on AI hardware, it doesn’t subtract that cost all at once; it spreads it over years, assuming the kit stays useful for a while. If the hardware actually goes stale quicker than the spreadsheet assumes, today’s profits look better than they really are — and those are the same profits being used to justify the borrowing. It’s not a scandal. It’s an assumption, sitting in a footnote, that may turn out to be generous.

The second is that some of the “demand” runs in a circle. A chipmaker invests in a young AI company, and the young company turns around and spends that money renting the chipmaker’s chips. On each set of books it reads as growth. Step back, and part of it is the same dollar going around a loop. Circular revenue is still revenue, right up until someone tests the circle.

None of this says AI is a fad, and none of it is a tip on what to buy. It’s a lens. When a boom is on, ask the boring question first: who gets paid no matter what happens? Lean toward clear cheques over hoped-for ones, and treat revenue that’s really money chasing its own tail with a little suspicion. Monday was the market asking that question out loud for the first time in a while. Which names we think it favours, and what we’re doing about it, is the desk’s work at moatpeak.com.

Free weekly letter and explainers like this; the daily research, levels and the Daily Compass are at moatpeak.com.

Educational research only — not investment advice. MoatPeak Group, UAB.