Your "momentum" fund is just an AI fund in disguise.

There's a comforting story we tell ourselves about factor investing — that it's the smart, diversified, rules-based way to own the market. One number this week quietly detonated part of it.

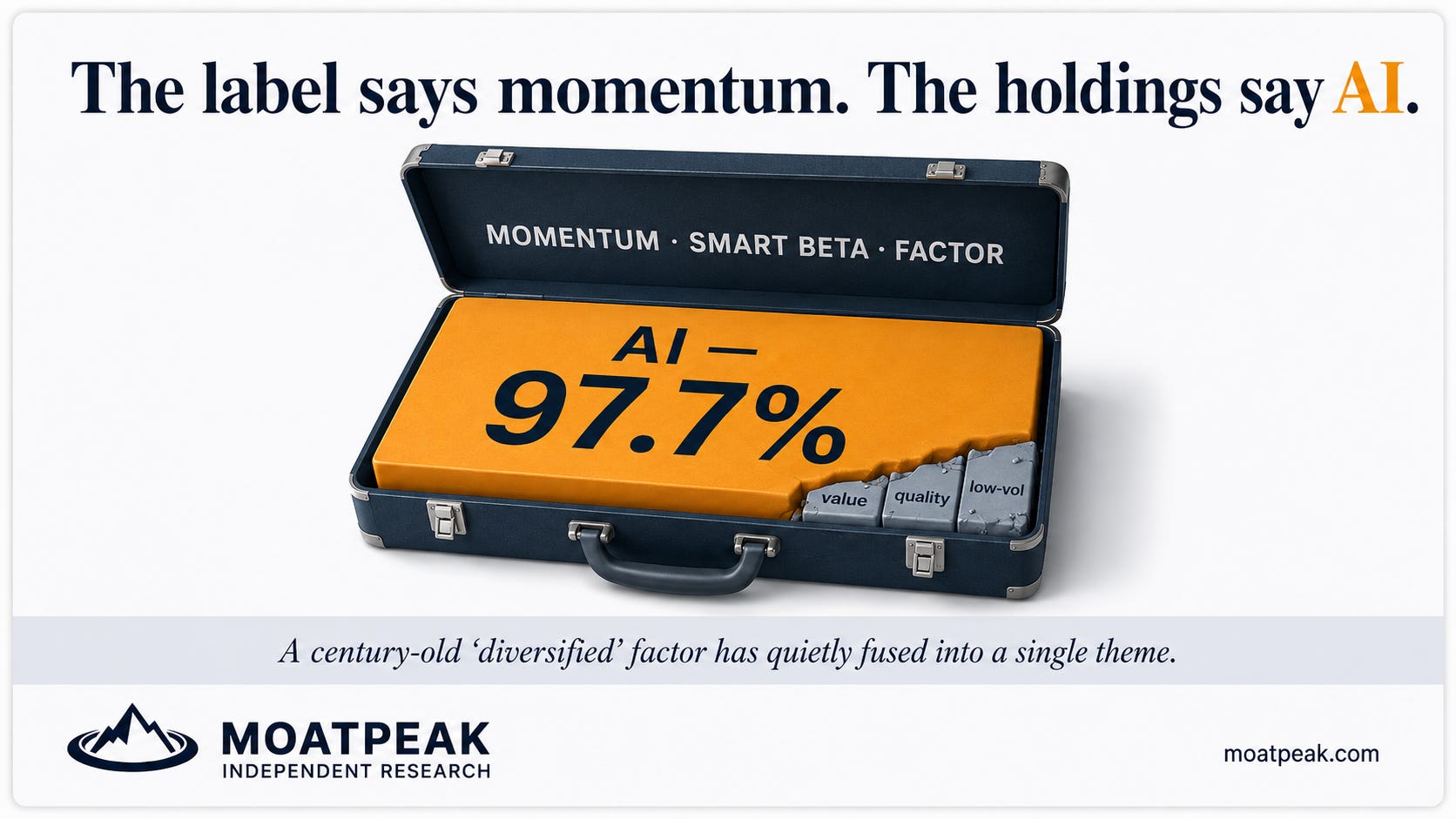

There’s a comforting story we tell ourselves about “factor” investing: that it’s the grown-up, rules-based, diversified way to own the market — momentum, value, quality, low-volatility, each a separate engine humming along on its own logic. This week a single number quietly blew a hole in part of that story. One major bank’s trading desk measured the correlation between the momentum factor and the AI complex at 97.7%. Not fifty. Not seventy. Ninety-eight, near enough. Which means momentum, right now, isn’t really a diversified strategy at all. It’s an AI bet wearing a lab coat.

Start with what momentum is supposed to be. It’s a mechanical rule: buy what’s been going up, sell what’s been going down, and stay completely indifferent to the story behind any of it. That’s the whole pitch — you’re not gambling on a narrative, you’re harvesting a statistical pattern that’s paid out across a century of market history. It’s meant to be the opposite of a hot-theme punt. That reassurance — “this is disciplined, this is diversified, this is not a bet on the thing everyone’s excited about” — is exactly what a 97.7% correlation quietly guts.

Here’s how the fusion happened, and it’s almost innocent. For two years, the thing that has been “going up” is, overwhelmingly, one theme. So the momentum machine, doing precisely what it was built to do, kept buying more and more of the same handful of AI-exposed winners — until “the stuff with momentum” and “the AI complex” became, statistically, the same basket. The factor didn’t malfunction. It did its job flawlessly, and its job walked it straight into a single crowded room. That’s how factor crowding always ends: the factor’s identity slowly dissolves into whatever theme is dominant, and one day you look up and you’re holding concentration you were sold as diversification.

Now the uncomfortable translation for your own account. If you own a fund with “momentum,” “smart beta,” or “factor” in its name, there’s a real chance you’re holding an AI concentration product you never consciously bought. And the galling part is that you got there by doing the responsible thing. You diversified away from picking individual stocks; you handed your money to a disciplined, back-tested, rules-based process — and the discipline marched you into the most crowded trade on the board. Go read the top ten holdings of that fund. If they look like a roll-call of the AI leaders, that isn’t a coincidence. That’s the 97.7% staring back at you.

So the lesson is the same one that keeps mattering in different costumes: diversification is not a label you purchase, it’s an outcome you have to keep re-checking. A strategy can be immaculately diversified in theory and quietly concentrated in practice, because the market drifted underneath it while the name on the tin never changed. The only defence is boring and unglamorous — periodically ask not “how many things do I own?” but “how many genuinely different questions am I betting on?” For a lot of “diversified” quant money right now, the honest answer is one. And when a trade this crowded eventually unwinds — they always do — it tends to tear apart from the inside, as the dispersion within AI itself finally pulls that correlation back down to earth.

A strategy can wear the full costume of diversification and still be a single bet underneath. The label says momentum. The holdings say AI. When those two disagree, believe the holdings.

Free weekly letter and explainers like this; the daily research, levels and the Daily Compass are at moatpeak.com.

Educational research only — not investment advice. MoatPeak Group, UAB.