Risk has two dials. Most people only watch one of them.

How often something goes wrong is the dial you feel. How badly it goes wrong when it finally does is the dial that empties the account — and right now it's flashing.

Picture two drivers. The first has a little fender-bender roughly once a year — irritating, cheap, quickly forgotten. The second hasn’t had so much as a scrape in a decade, but when they finally do crash, it’s a total write-off. Which one is the riskier driver? Most of us instinctively point at the first, because their trouble happens often and we can picture it. But risk always comes with two separate dials — how often something goes wrong, and how badly when it does — and it’s usually the second, quieter dial that does the real damage.

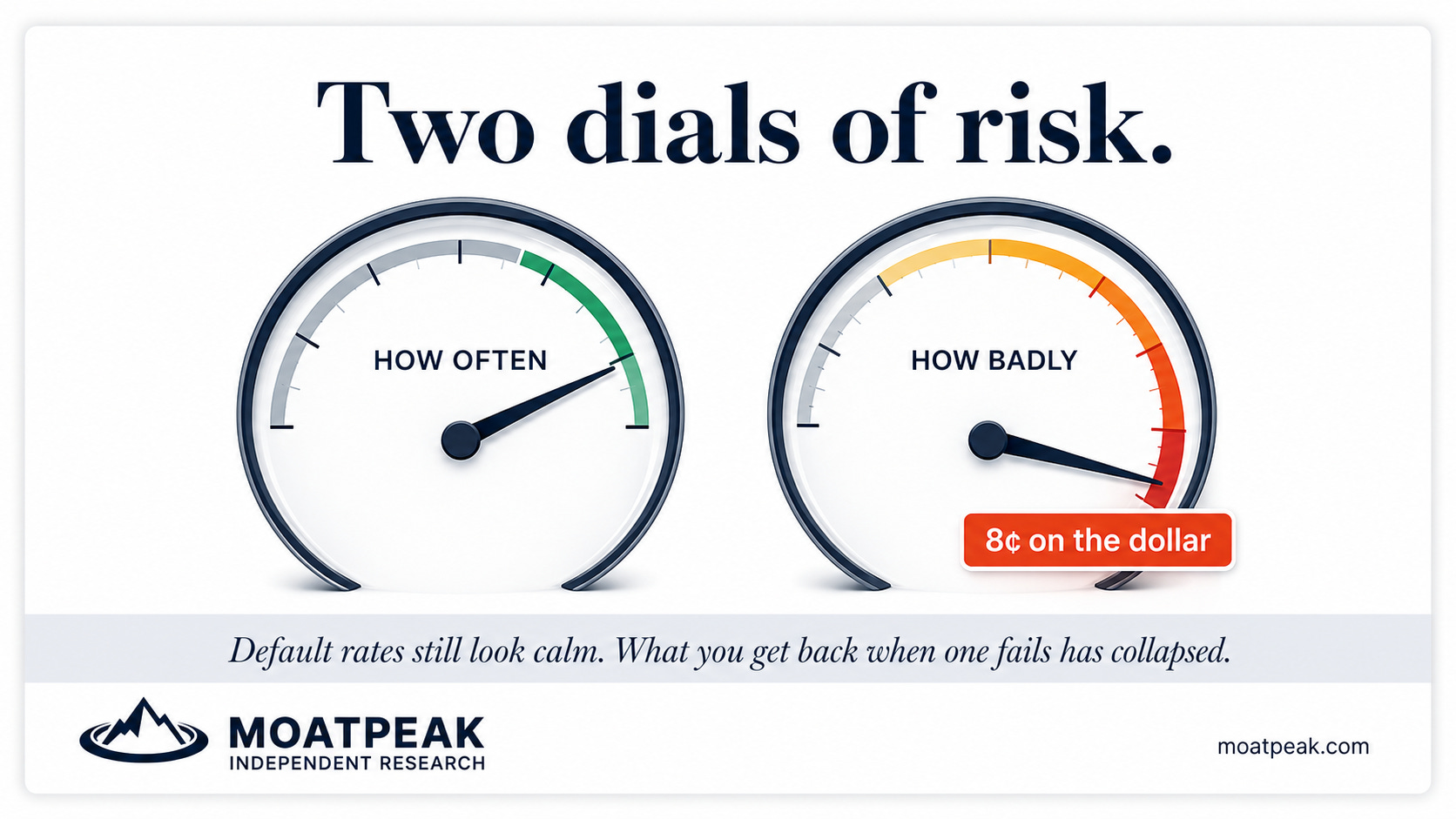

Markets are running a near-perfect example of this right now, and it makes the idea concrete. In Europe, the rate at which junk-rated companies default on their bonds still looks low and calm — the “how often” dial reads a reassuring green. But the other dial has quietly gone haywire. When a European junk bond actually does default now, investors are getting back only around 8 cents on the dollar — down from roughly 41 cents just a year earlier. The frequency looks fine. The severity has fallen off a cliff. Same asset, two completely different messages, depending on which dial you read.

Why does that particular pairing matter so much? Because it’s a classic late-cycle fingerprint. When money is easy and everyone’s feeling optimistic, lenders tend to “extend and pretend” — they keep a struggling borrower alive with fresh loans rather than let it fail, which keeps the number of defaults flatteringly low. But the business underneath quietly rots the whole time, so that when it finally does collapse, there’s almost nothing left to hand back. Low frequency, catastrophic severity. The calm dial is calm because the damage is being postponed, not because it’s being avoided. The quiet isn’t reassurance; it’s a symptom.

Now the part that’s actually worth keeping, because this was never really about European bonds. It’s about how to judge any risk at all — including your own decisions. A strategy that “wins nine times out of ten” sounds wonderful right up until you notice that the tenth time takes everything you made on the other nine. A portfolio that’s been placid for years isn’t automatically safe; it may simply be storing severity for later. The right question is almost never “how often has this gone wrong before?” It’s “what does one bad outcome actually cost me — and could I survive it?”

There’s a reason we get this backwards so reliably, and it’s worth naming. Our brains are built to track frequency, because frequency is what we feel day to day — the small, regular knocks. Severity stays abstract, a story we tell ourselves, right up until the moment it arrives and becomes the only thing that matters. The investors who genuinely blow themselves up are rarely the ones who misjudged how often trouble comes. They’re the ones who were right about the odds and catastrophically wrong about the size.

Frequency is the dial everyone watches, because it’s the one that twitches and fidgets and keeps you company. Severity is the dial that empties the account — and it tends to sit perfectly, deceptively still, right up until the moment it doesn’t.

Free weekly letter and explainers like this; the daily research, levels and the Daily Compass are at moatpeak.com.

Educational research only — not investment advice. MoatPeak Group, UAB.