The biggest safety net under markets isn't the Fed anymore. It's the state.

When a government decides an industry is too important to fail, it changes the risk of owning it — in one obvious way, and one that almost nobody prices.

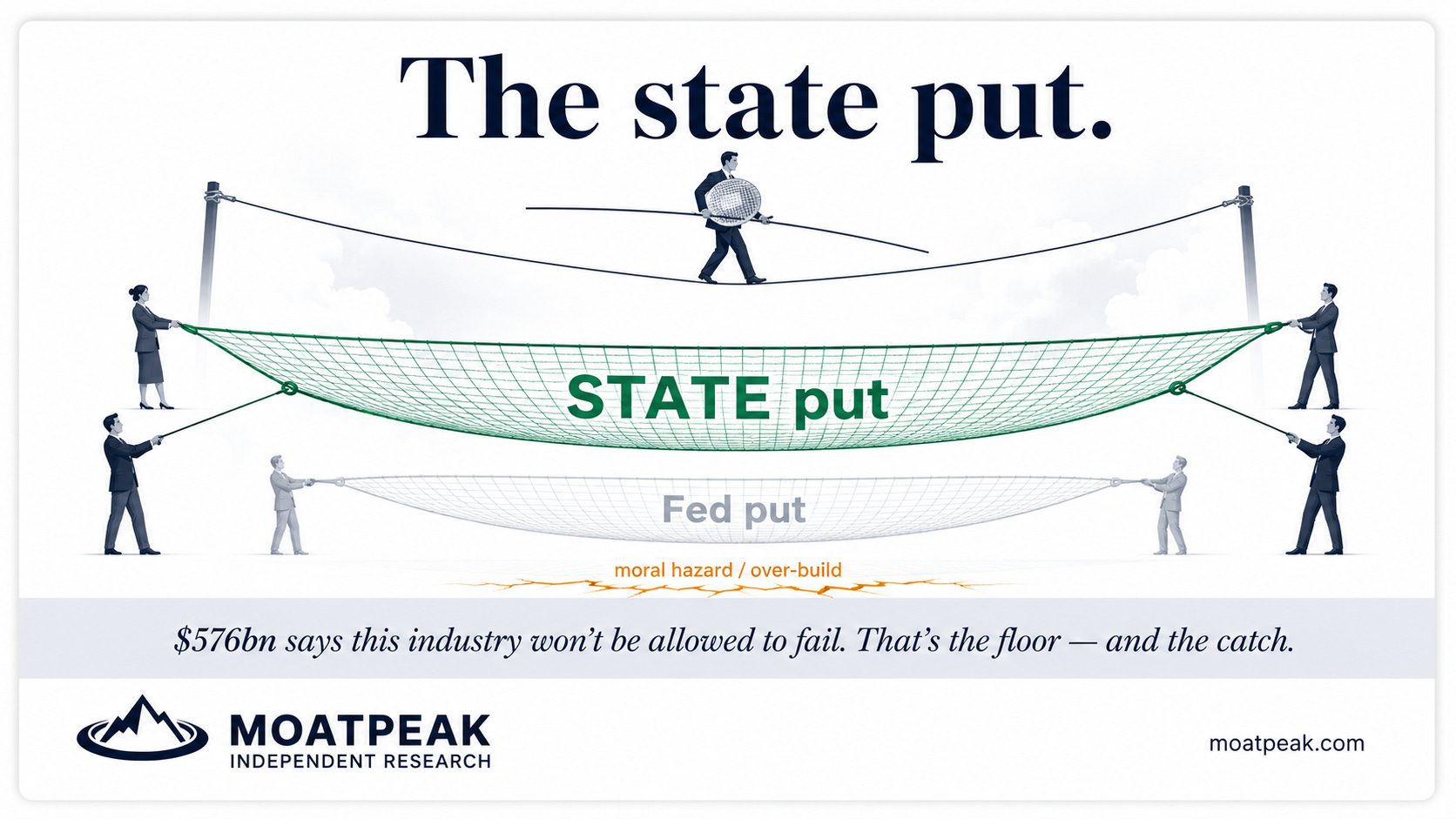

For a whole generation, investors leaned on an invisible safety net nicknamed the “Fed put” — the belief that if markets ever fell far enough, the central bank would ride in with lower rates and catch everyone. You didn’t have to see it to rely on it; it quietly shaped how much risk people were willing to take. Something bigger and stranger is now being strung underneath certain industries, and it’s worth understanding before you lean your weight on it — or get blindsided by it.

Call it the state put. When a government decides an industry is not merely profitable but strategically essential — a matter of national security, or national survival — it stops treating that industry like an ordinary business and starts treating it like critical infrastructure, the way it treats bridges or the power grid. This summer served up a textbook case. South Korea committed to a state-orchestrated investment programme worth around $576 billion — new chip factories, packaging clusters, AI data centres — built around its two great memory-chip champions, with the president standing personally beside their leaders to announce it. That is a government declaring, in hard currency, that this industry will not be permitted to fail.

You could see the psychology of it play out just days later. When those very chip stocks suddenly plunged — a brutal two-day drop severe enough to trip an emergency halt on Korea’s market — they clawed back most of the loss within about forty-eight hours. I want to be careful here: I’m not claiming the investment programme “caused” that bounce, and the timing doesn’t even line up that neatly — markets are far messier than a single cause. The point is subtler and more durable. When investors believe an industry is sitting on a national safety net, they buy the dips faster and panic less, because they sense that someone with a printing press and a political mandate is standing somewhere underneath. The floor never has to be tested to change how people behave. Simply believing it’s there is enough.

And here is the contrarian twist — the reason this is a double-edged thing rather than simply good news. That same safety net that cushions the fall is also moral hazard, the oldest problem in all of finance. If a company, or an entire national industry, comes to believe it will be caught, it starts to take bigger risks: it borrows more, builds more aggressively, worries less about the drop. So the state put doesn’t actually remove risk from the system. It changes its shape — less risk of a clean, cathartic crash, and more risk of a slow, subsidised over-build that quietly inflates until something further down the chain gives way instead. You’ve traded a sharp pain you can see for a soft distortion you can’t.

Which means the practical lesson is not the cheerful “strategic industries are safe now.” It’s this: know which kind of thing you actually own. Are you invested in something a government has quietly decided it must defend — chips, defence, a few systemically important banks — which comes bundled with a hidden floor and a hidden distortion? Or in something it would happily let fail? Those two carry completely different risks even when their charts look identical. The costly mistake is assuming the net is strung under your seat, when it was only ever tied beneath the parts the state has decided are essential.

A floor you didn’t pay for feels like a gift. But a backstop whose price you can’t see isn’t the same thing as safety. It’s just a risk that’s been quietly moved somewhere you’ve stopped looking.

Free weekly letter and explainers like this; the daily research, levels and the Daily Compass are at moatpeak.com.

Educational research only — not investment advice. MoatPeak Group, UAB.