The crash is real. The cause is leverage. The calm is borrowed.

The AI trade fell hard today. Here is our actual daily read, decomposed with the real screenshots: a mechanical unwind under a stretched rubber band, not a fundamental break.

Today the most crowded trade on earth fell hard. Semiconductors are near a bear market, the SOX down about a fifth from its June high. Micron is off roughly 30 percent from its peak. In Seoul, more than 1.2 million leveraged retail accounts were hit with margin calls and hundreds of thousands were force-sold, the KOSPI down about a quarter from June. The internet split into the two reactions it always splits into: the bubble has burst, sell everything, versus buy the dip, it is fine.

We think both are wrong, and we can show you exactly why, because we publish a read on this every single trading day. It is called the Daily Compass. Here is today’s, taken apart, with the actual screenshots.

Start with the number. The Compass Reading is our one proprietary gauge of how defensive to be, a composite of five things we can measure: crowding, breadth, leverage and flows, liquidity and rates, and equity supply. Today it sits at 76 out of 100, in the defensive band, nudged up a single point. The nuance is the whole point. We raised our guard because the unwind turned mechanical, but we did not jump to a crisis reading, because the demand underneath is intact and the broad market is calm. A gauge that only ever screams is useless. The work is in the one-point move.

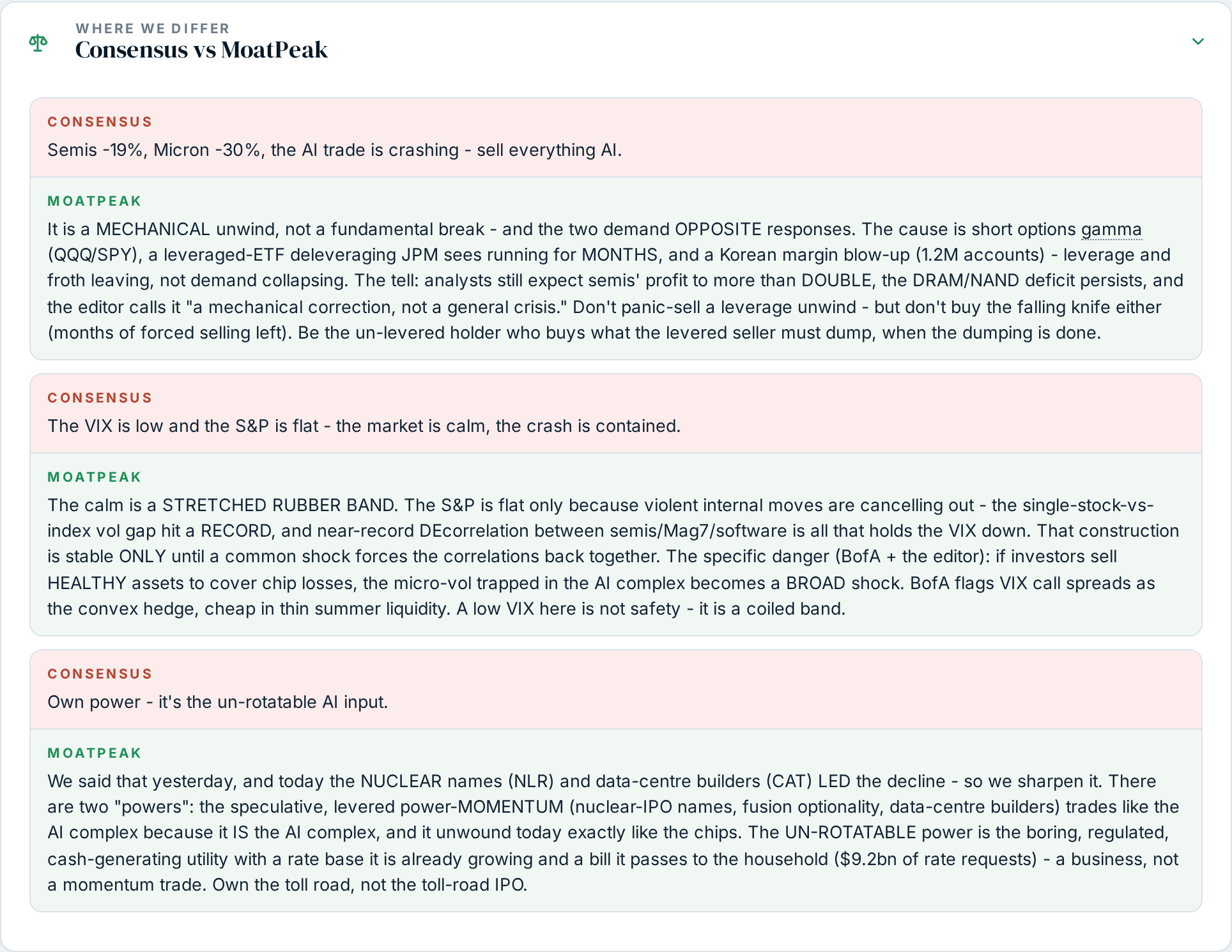

Now the contrarian core, the reason we are not selling everything. This is a mechanical unwind, not a fundamental break, and the two demand opposite responses. Three forces are doing the selling, and none of them is a customer cancelling an order. Dealers are short options gamma in the big index ETFs, which forces them to sell into every down move. A leveraged-ETF deleveraging that JPMorgan expects to run for months is still grinding through. And Korea’s retail margin blow-up is mechanically dumping stock regardless of price. The tell that this is froth and leverage leaving, rather than demand collapsing, is that analysts still expect the sector’s profit to more than double and the memory shortage to persist. Even the wire coverage today called it a crowded-trade correction, not a fundamental deterioration. So we lay our view directly against the consensus, line by line.

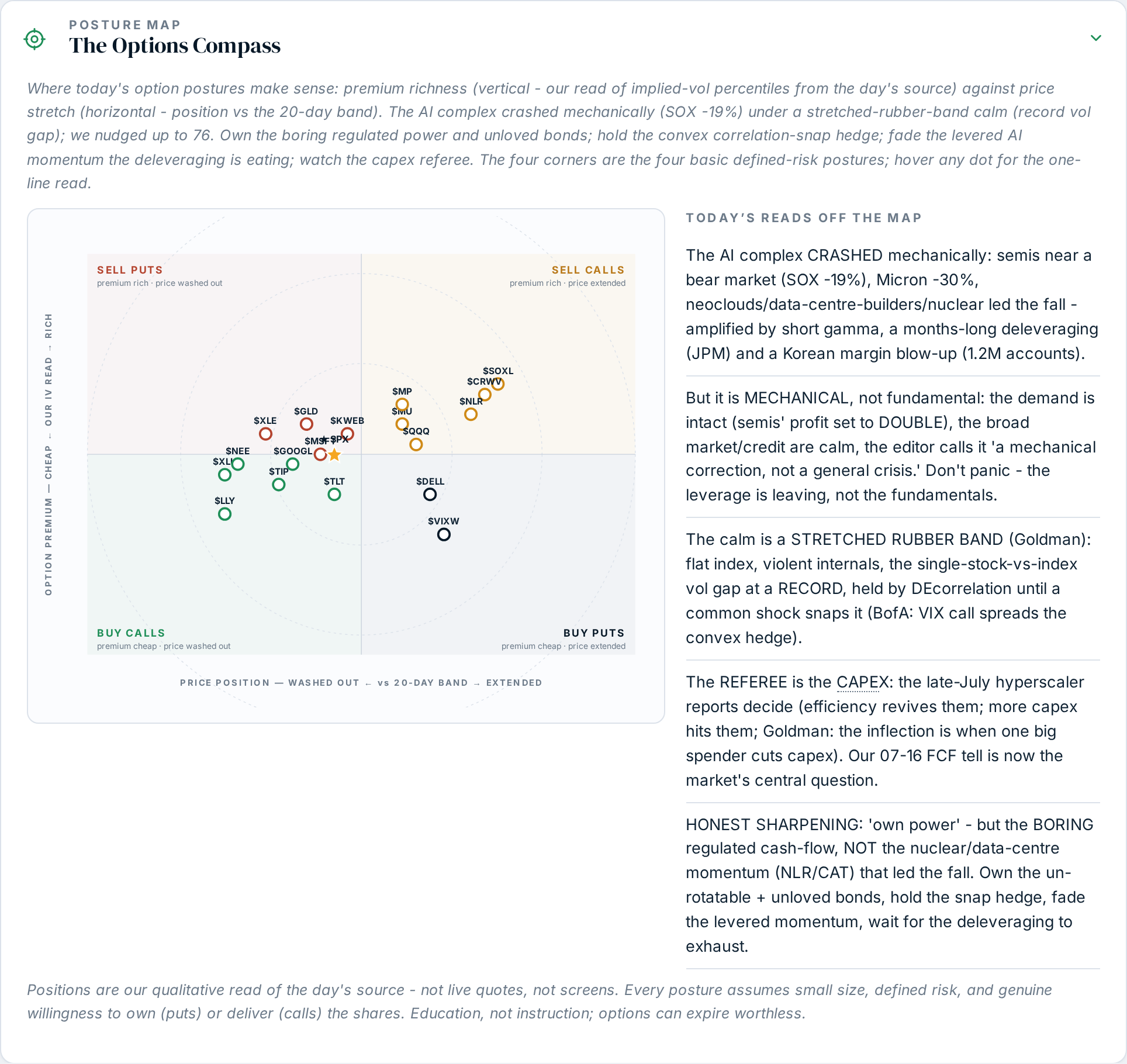

Then the part almost nobody is pricing: the calm above the crash is borrowed. The S&P barely moved today while its internals convulsed, and there is a mechanical reason. Since June, the correlation between the big AI names has collapsed from about 80 percent to roughly 20 percent, and the gap between single-stock and index volatility has hit a record. In plain terms, the violent moves are cancelling each other out, so the index looks serene while the names inside it are on fire. Goldman’s image for this is a stretched rubber band. It holds only until a common shock forces the correlations back together, at which point the micro-volatility trapped inside the AI complex becomes a broad-market shock. A low VIX here is not safety. It is a coiled band. That is why we carry a convex hedge rather than trusting the quiet.

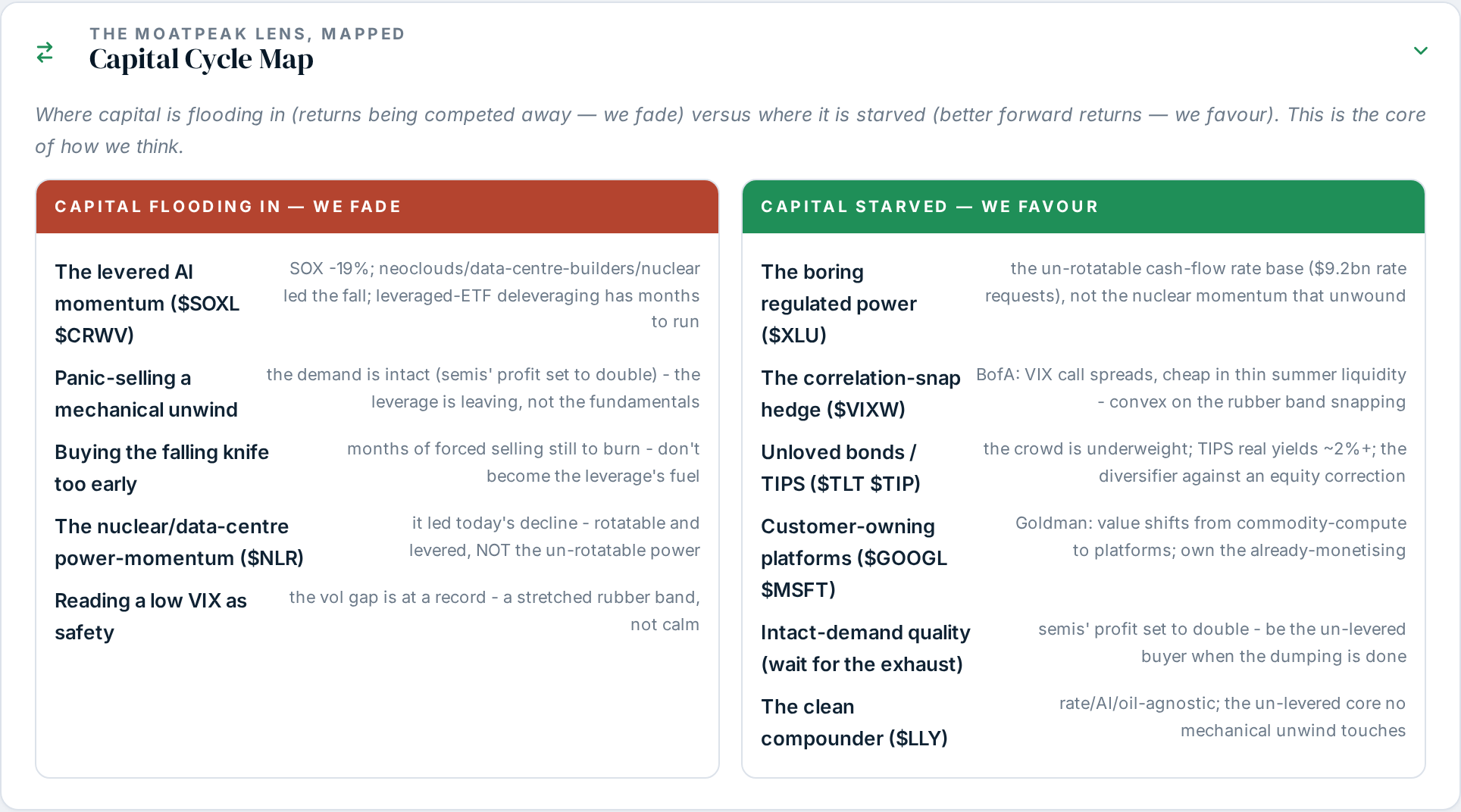

So where do we actually lean. This is the core of how we think, and we map it every day: where capital is flooding in and returns are being competed away, which we fade, against where capital is starved and forward returns are better, which we favour.

And here is the honest part, the one that builds more trust than any winning call. Yesterday we told readers to own the un-rotatable input to AI, which is power. Today the nuclear and data-centre-builder names led the decline. So we sharpened, in writing, same day: there are two powers. The speculative, levered power-momentum, the nuclear-IPO and fusion and builder names, trades like the AI complex because it is the AI complex, and it unwound with the chips. The un-rotatable power is the boring, regulated utility with a rate base it is already growing and a bill it passes to the household. Own the toll road, not the toll-road IPO. We mark our own homework the day the tape argues with us, not a month later when it is safe.

Expressing a defensive view without over-trading matters too, so we map the option postures rather than just naming stocks. The four corners are the four basic defined-risk stances, premium richness against how stretched the price is, so a reader can see where selling a put, or buying a cheap convex hedge, actually makes sense today.

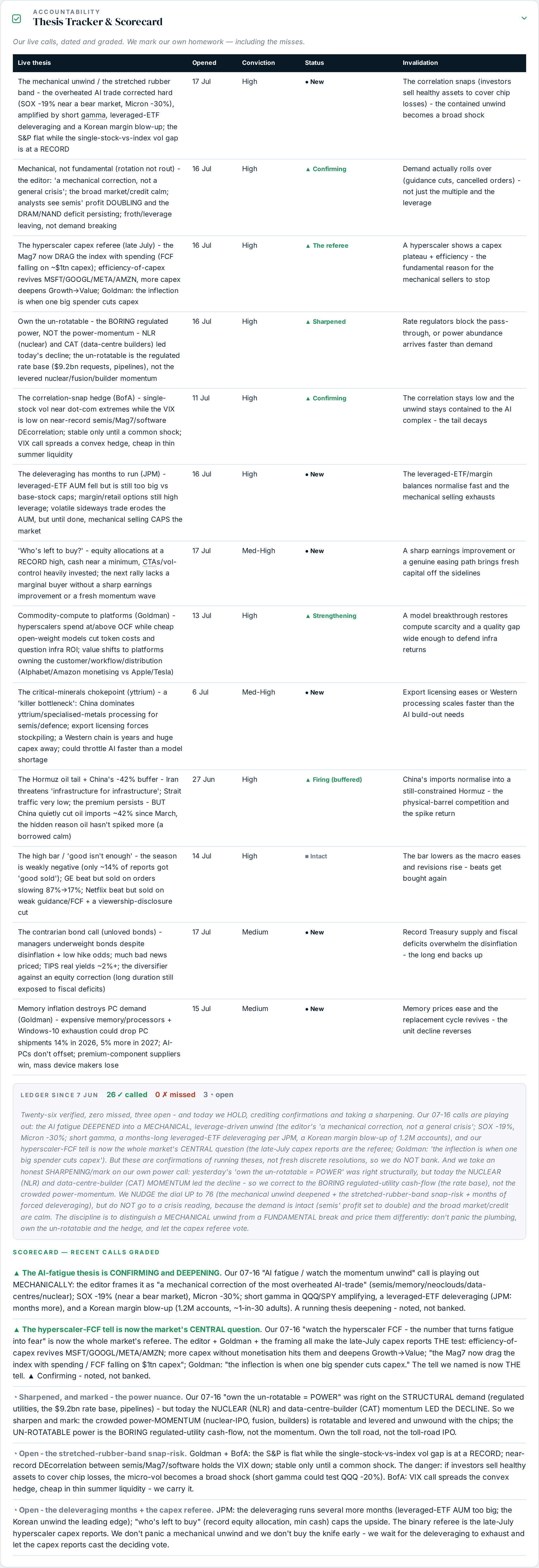

None of this means anything without a track record, so we keep one in the open. Every thesis is dated, graded and given the specific condition that would prove it wrong. We credit the confirmations and we flag the misses.

That leaves the one thing that ends or extends all of this: the referee. The market’s fear has flipped from too few leaders to too much spending, with free cash flow falling under the near-trillion-dollar-a-year the hyperscalers are pouring into AI. The late-July hyperscaler reports are the vote. A focus on the efficiency of what has already been spent revives the platform names. A commitment to keep accelerating spend without proven monetisation deepens the rotation out of expensive growth. Goldman’s line is that the inflection comes the day one big spender cuts capex. We are ten days from that vote, and until it lands the mechanical selling caps the tape.

That is one day of the Compass. We publish it every trading day at moatpeak.com: the live Reading, the eight sections behind these panels, the tripwires that tell us when the regime has actually changed, and the specific actions that follow. Today’s read, in one line: do not panic a mechanical unwind, because the demand is intact and the leverage is leaving. Own the un-rotatable and the unloved, hold the convex hedge for the snap, and let the capex referee cast the deciding vote.

Educational research only. Not personalised investment advice. MB “MoatPeak Group”.