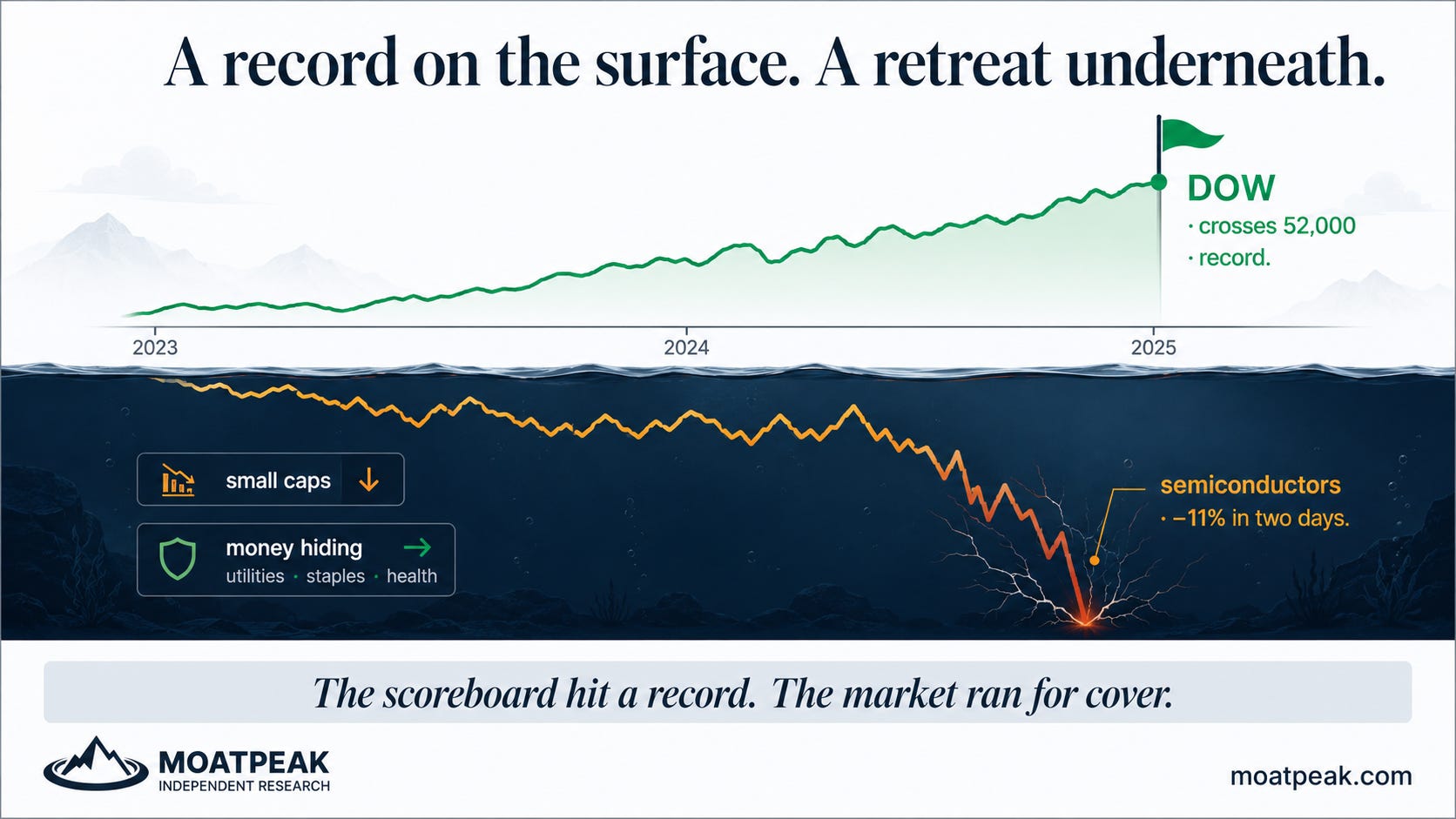

The Dow hit a record. Underneath, the market was running for cover.

It crossed 52,000 for the first time this week — while the chips powering the whole AI boom fell about 11% in two days. A record built on a retreat isn't strength. It's the warning.

This week the Dow crossed 52,000 for the first time in its history and closed at one record after another. Read only that sentence and it sounds like a triumph. Now read the second one: the semiconductor stocks that have powered this entire bull market fell about 11% in two days. Same market, same four trading days, opposite directions. When the scoreboard and the engine disagree that violently, the scoreboard is the part to distrust.

A record high is supposed to mean confidence — lots of companies doing well, money flowing in across the board. That isn’t what this was. Underneath the record, the money wasn’t spreading out; it was huddling up. Investors sold the exciting, economically-sensitive things — chips, smaller companies — and crowded into a handful of giant “safe” names and the dullest, steadiest corners of the market: utilities, household staples, health care. That’s not an everything-rally. It’s the portfolio version of moving to higher ground. A record made by everyone crowding through the same few doors isn’t strength. It’s fear wearing a party hat.

Two things give the game away. The first: while the Dow set records, the index of small companies actually fell. Small caps are the part of the market tied most tightly to the ordinary domestic economy, and they didn’t get the invitation to the party. The money that did move went hiding — into the sectors you buy when you want shelter, not the ones you buy when you’re optimistic. When the leaders of a “record” week are the electric utility and the toothpaste maker, the market is telling you something it isn’t saying out loud.

The second tell is quieter and harder to wave away. A weak jobs report — and this week’s was weak, barely half the hiring forecasters expected — normally pushes longer-term interest rates down, because slower growth means cheaper money ahead. This time the long end refused to fall, and the yield curve steepened instead. In plain terms: the bond market looked at the very same weak jobs number the stock market was cheering and drew the opposite conclusion. Not “the Fed will ride to the rescue,” but “growth is cooling and the costs aren’t.” When stocks and bonds read one fact in opposite directions, bonds are usually the one worth believing.

Underneath all of it, the story that has carried this whole market took its first real hit. For two years the case for anything with “AI” attached rested on a single word: scarcity. Computing power was supposedly endlessly scarce, so whoever made the chips could name their price. Then this week Meta — one of the very biggest buyers of those chips — signalled it might start selling its spare computing capacity back to everyone else. A shortage story dies the instant its biggest hoarder turns into a seller. That is what the chip crash was really pricing: not a bad few days, but the first crack in “shortage forever.”

It’s also worth knowing how the calm surface got manufactured, because it makes the calm harder to trust. A couple of the market’s giants quietly papered over the damage — a jump in Apple on product-pipeline buzz did a lot of the index’s heavy lifting, holding the average up while the typical stock sank beneath it. And the “good news” wasn’t always what it looked like: one carmaker reported record deliveries and the stock fell anyway, because the market finally looked past the volume to the margin it cost to get there. A record you have to squint to believe is a record worth squinting at.

So the useful way to read a week like this one isn’t “Dow record, all clear.” It’s almost the reverse. Put a single question to any strong tape: is the strength broad — plenty of ordinary companies rising, real confidence — or is it narrow, a few safe giants holding the average up while everything else quietly leaks away? This week it was narrow, and narrow strength is the fragile kind. None of that is a reason to bolt for the door. It’s a reason to notice which market you’re actually looking at: the one on the scoreboard, or the one underneath it. The levels and the odds are ours to trade. The shape of the week is yours to keep.

Free weekly letter and explainers like this; the daily research, levels and the Daily Compass are at moatpeak.com.

Educational research only — not investment advice. MoatPeak Group, UAB.