The longevity industry isn't selling you more life. It's selling you doubt.

A new deep dive, decomposed with the real slides. In the wellness boom the rent goes to the platform that owns your data, not the drug or the lab, through a subscription loop of measurement and doubt.

Silicon Valley money is pouring into living forever, and most investors think the way to play it is obvious: buy the anti-aging moonshot drugs, or, if you want the safe version, buy the “shovels,” the laboratories that process everyone’s blood no matter which therapy wins. Our new thematic deep dive argues that both of those instincts are wrong, and it says so in a single, uncomfortable sentence. Here is the report, taken apart, with the actual slides.

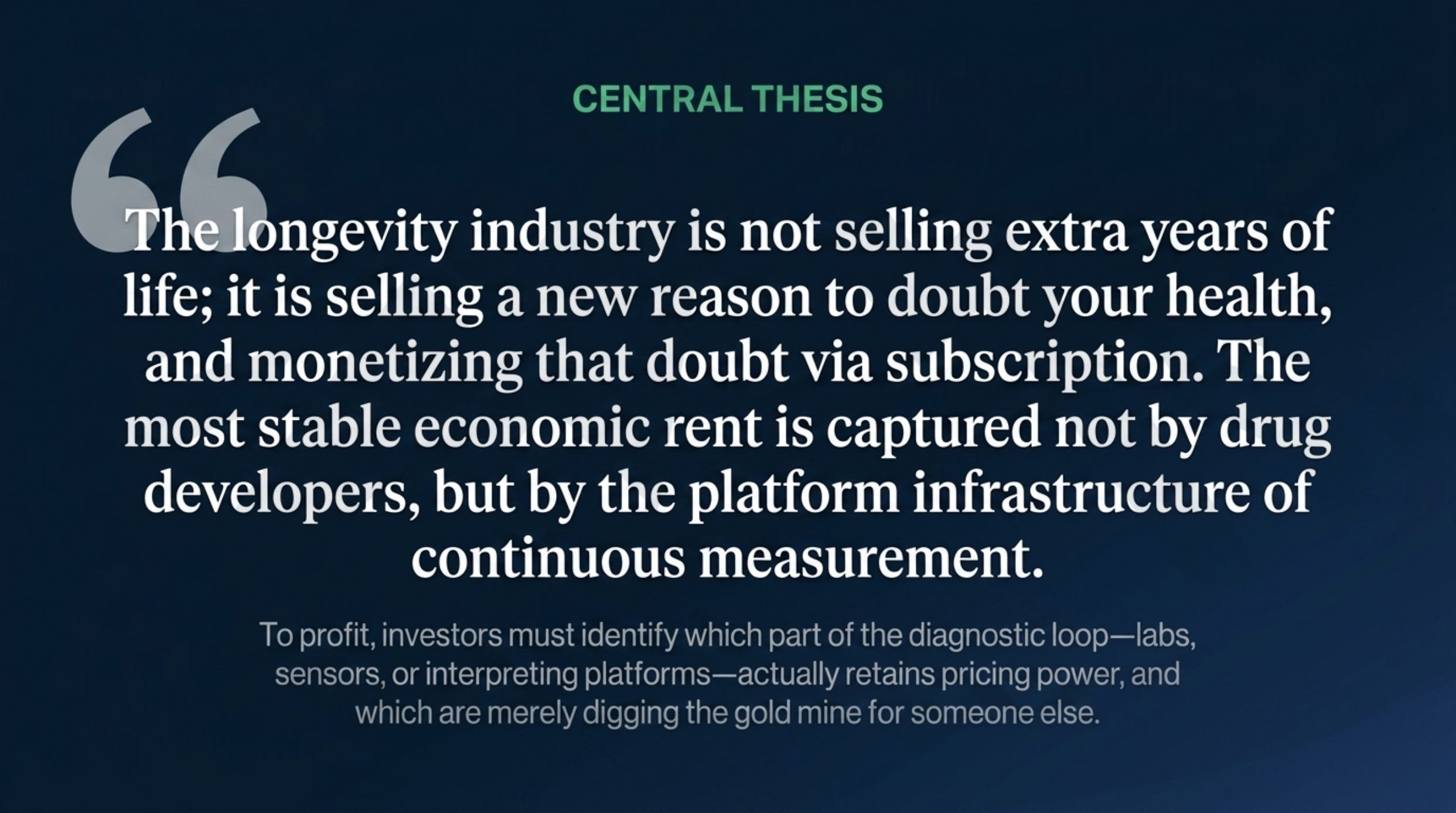

That is the whole thesis. The longevity industry is not, mostly, selling you extra years of life. It is selling you a new reason to doubt your health, and then monetizing that doubt through a subscription. We call it the Subscription Loop, and it runs in four steps. A sensor or a blood test measures a biomarker and flags it as outside an “optimal” range, a range often narrower than what your doctor would call normal. A dashboard turns that into a small red notification, and a little anxiety. You seek an interpretation through a connected telemedicine service. A protocol is prescribed, and a follow-up test is ordered to check whether it worked. Then the loop starts again. The company that owns the interpretation and the data history owns the customer. The laboratory that actually spins the blood is a subcontractor. The platform is the landlord.

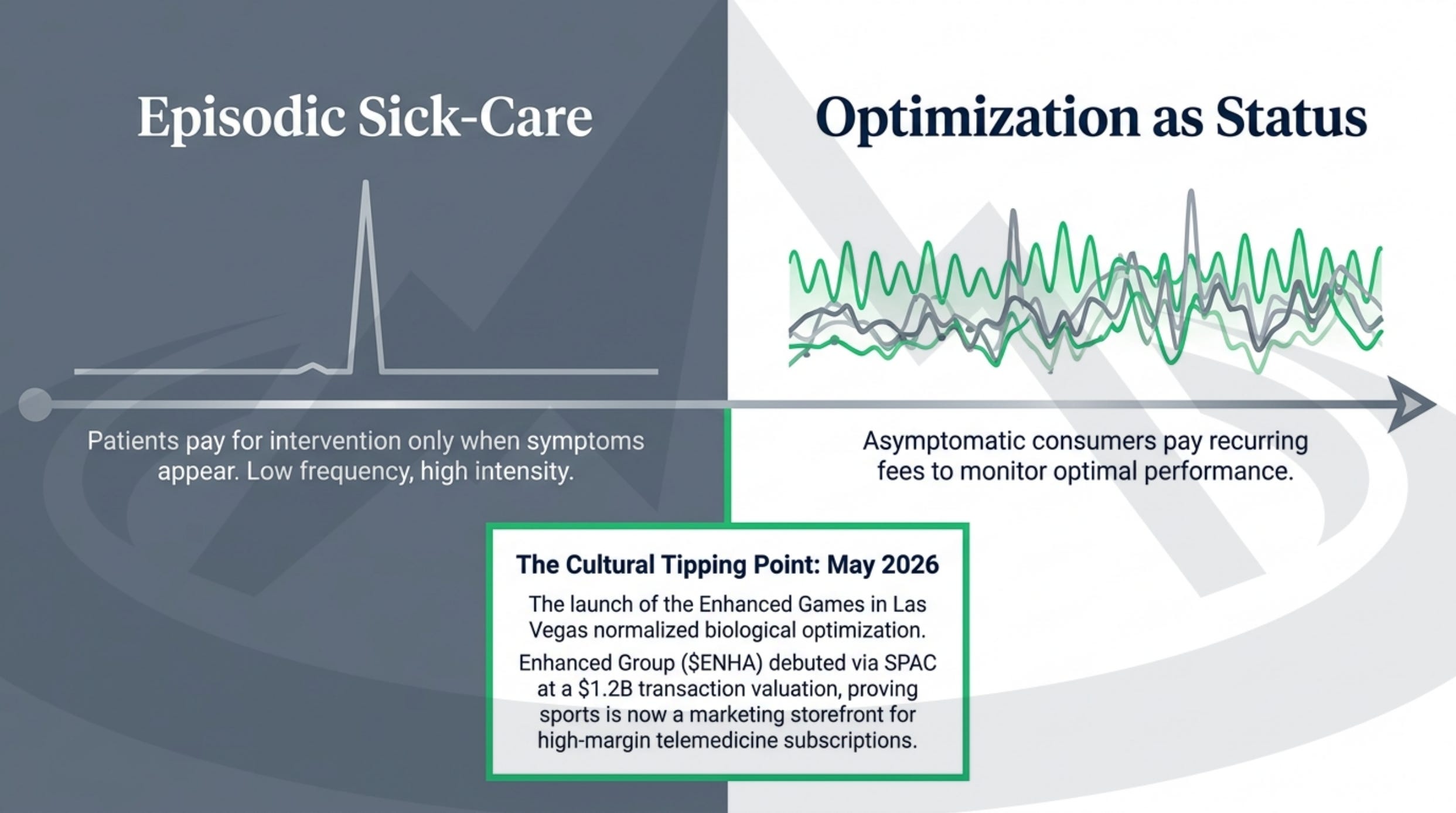

Why now, and why this is not just another biotech cycle. The demand has shifted from episodic sick-care, where you pay only when something hurts, to optimization as status, where healthy people pay a recurring fee to monitor how optimal they are.

Three 2026 events turned that culture into an asset class. Abbott closed a roughly 20.6 billion dollar acquisition of Exact Sciences, the maker of Cologuard, funded mostly with 20 billion dollars of new debt, which turns cancer screening from a science project into core infrastructure. A new Multi-Cancer Early Detection Act created a Medicare pathway for advanced screening. And the Enhanced Games, the performance-enhanced sporting event in Las Vegas in May, listed its parent through a roughly 1.2 billion dollar deal, with a storefront selling peptides and longevity protocols attached. That last one is instructive on its own terms: the stock fell around 70 percent after the event flopped, which tells you the culture is real but the equity is a mood, not a business.

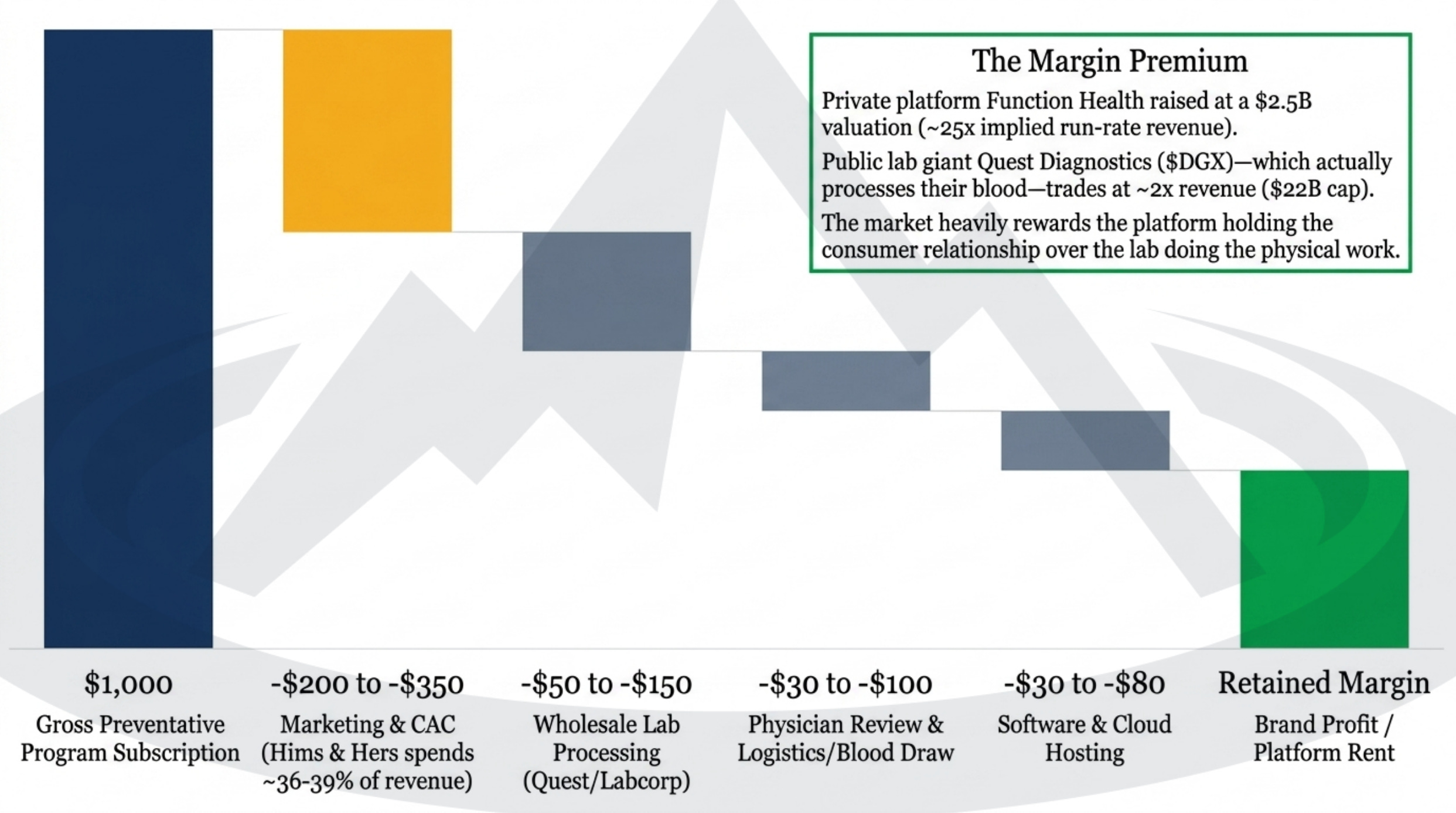

Now the first uncomfortable number. Investors are paying wildly different prices for the same blood. Function Health, a private platform, raised at a 2.5 billion dollar valuation on roughly 100 million dollars of revenue, somewhere around 25 times sales. Quest Diagnostics, which runs much of the actual testing behind platforms like it, trades at about 2 times sales. The market is treating the app that reads your blood as a software company and the lab that draws it as a utility. Watch where the dollar in your subscription actually goes.

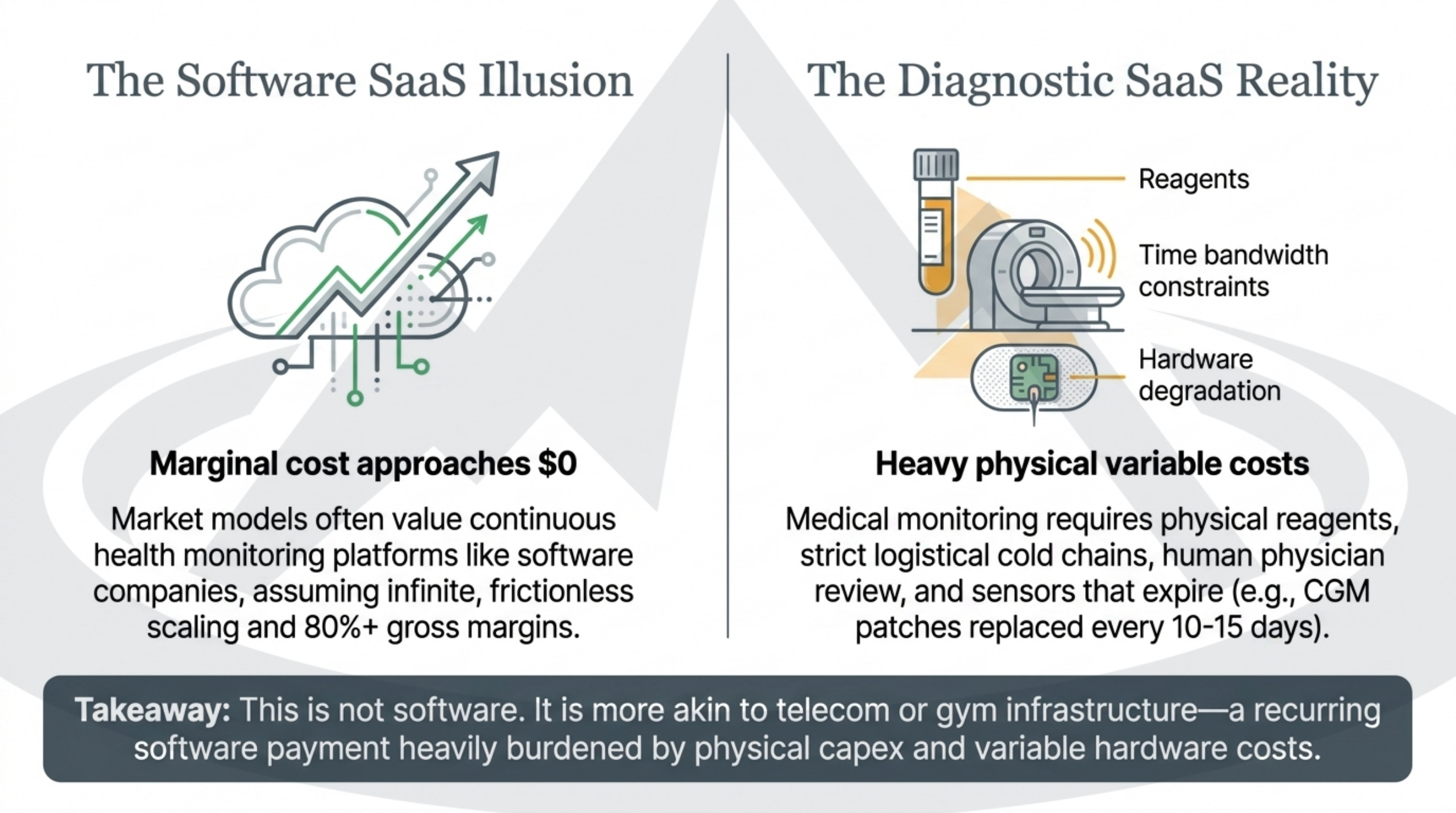

Here is why we think that premium is partly a SaaS illusion. Real software has near-zero marginal cost. Medical monitoring does not. Every test burns reagents, shipping, a phlebotomist, and a clinician’s time to review it, and the sensors physically expire and get replaced. After those costs, gross margins land closer to 30 to 50 percent than to the 80 to 90 percent of a true software business. This is not software. It is closer to a gym or a telecom: a recurring subscription sitting on top of real, physical infrastructure.

So if the margins are ordinary, where is the moat? In lock-in. Once you have three years of blood history on one platform, leaving means losing the baseline that makes every future reading meaningful. The switching cost is your own past. That, not the margin, is what the valuation is really paying for.

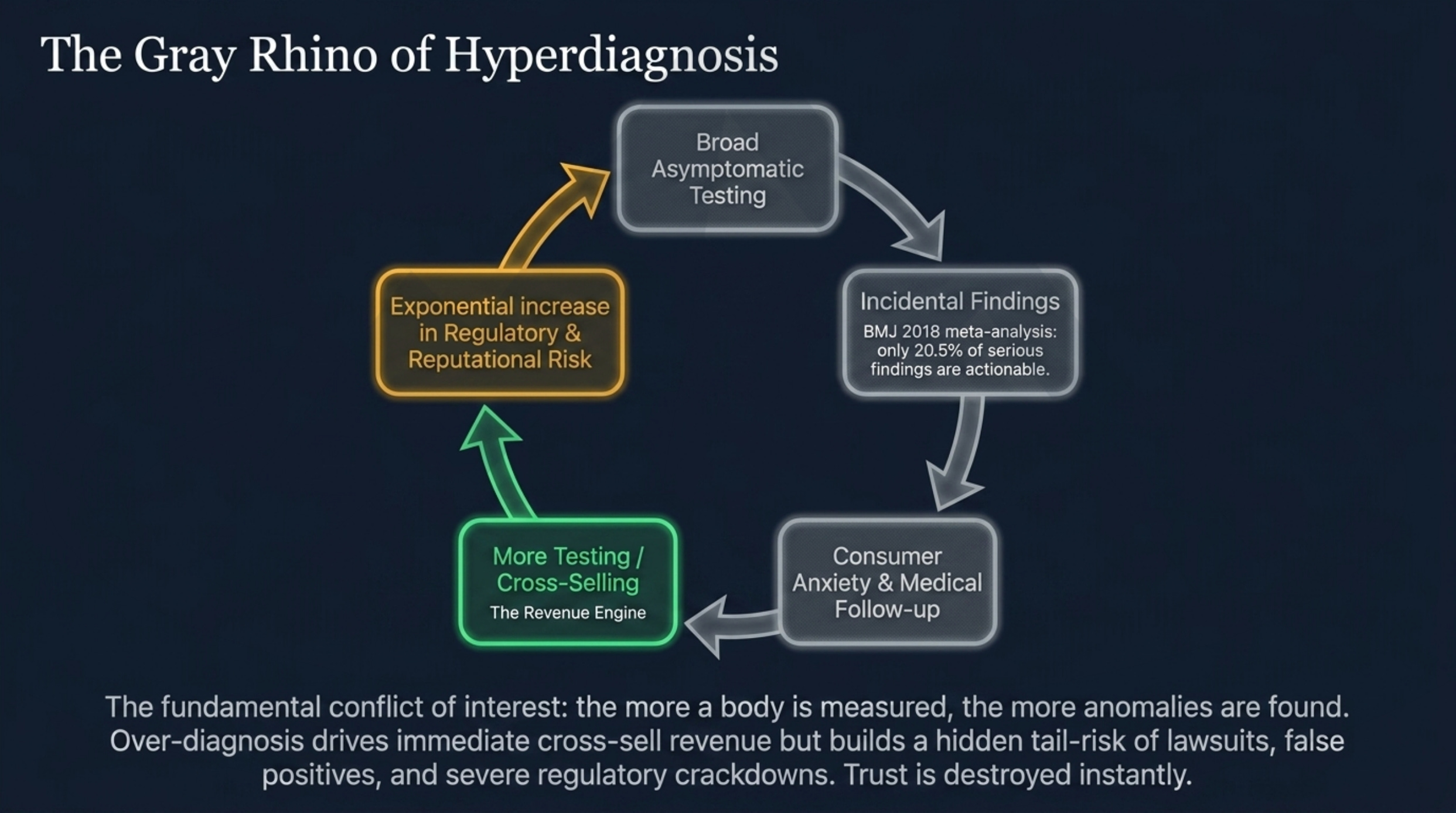

Now the engine, and the part that deserves a public flag. The growth driver of this whole category is what we call hyperdiagnosis: measure more of a healthy body, and you will find more anomalies. The trouble is that most of what broad scanning finds in people who feel fine is of uncertain significance. A large 2018 meta-analysis in the BMJ found that scanning asymptomatic adults turns up incidental findings in a meaningful share of them, most of them not clearly serious, and, in the authors’ own words, little is known about whether chasing them helps. But each finding still generates a real follow-up: another consult, another scan, another bill.

That is a marvelous revenue engine and a genuine tail risk at the same time. It pulls anxious, higher-cost consumers into the system first, it pushes private testing back into the insurance-covered world for treatment, and it hands the platform more information about your future than your insurer has. One well-publicized false positive, one lawsuit, one regulator deciding that “biological age” is a medical claim, and the trust that the whole loop runs on can evaporate overnight.

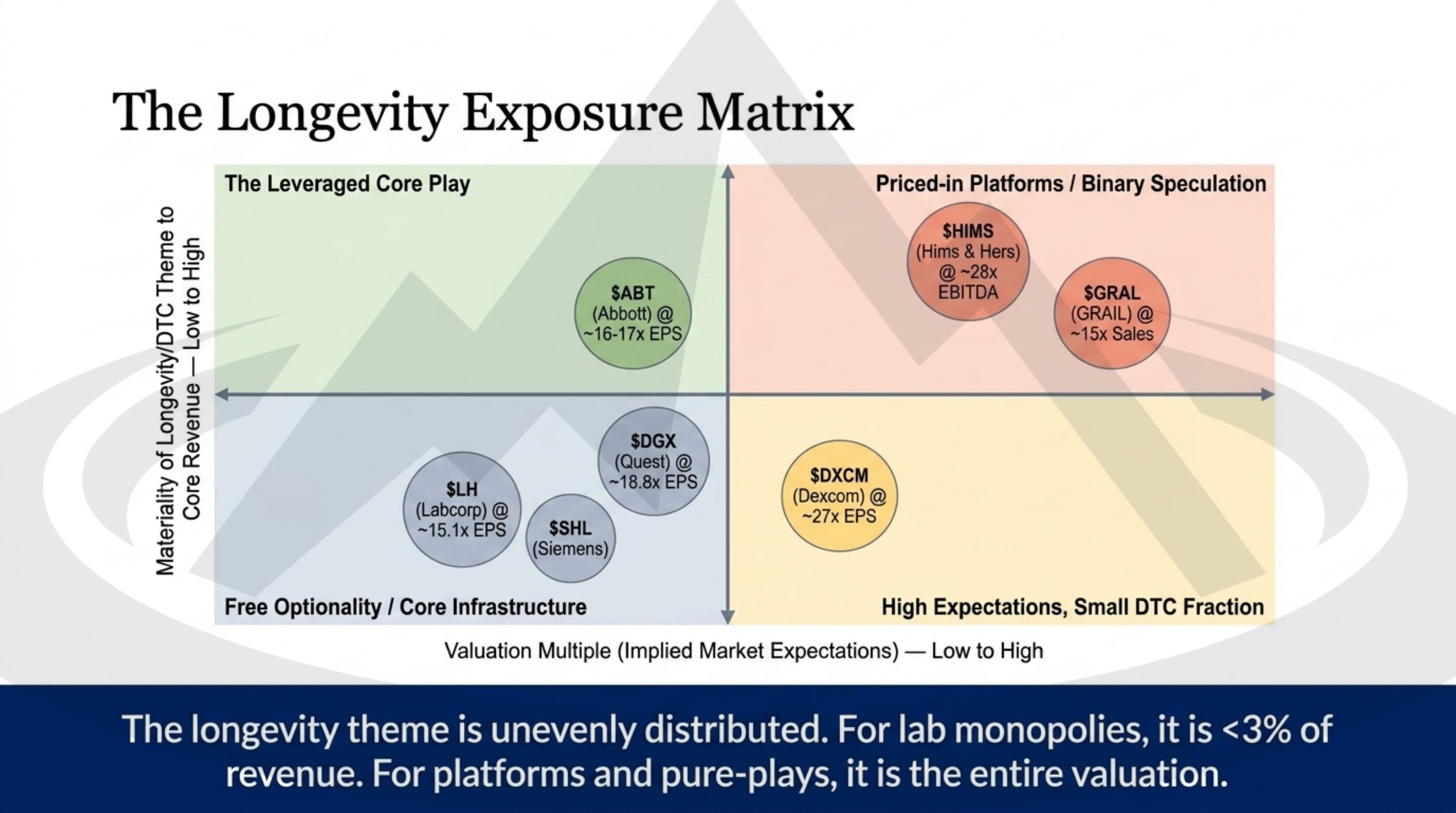

Where does that leave the actual stocks. Not evenly. This is the map we built, and the punchline is in the caption: for the lab monopolies, longevity is under three percent of revenue, a free lottery ticket on top of a mature cash-flow business. For the platforms and pure-plays, it is the entire valuation.

A few reads off that map, with the detailed valuation work held for the report. Abbott is the leveraged core play, real reimbursed scale in glucose sensors plus the new cancer-screening franchise, but now carrying around 34 billion dollars of debt, so the case rests on integration rather than hype. Hims and Hers is the interface personified, the storefront that owns the customer and is buying its way up the chain, including a 1.15 billion dollar deal for Eucalyptus, but its growth leans on a fragile transition in weight-loss drugs. GRAIL is the binary option: its Galleri cancer test missed the primary endpoint of the big NHS trial, even though it cut late-stage diagnoses, and the company burns cash while it waits on US reimbursement. The labs, Quest and Labcorp, are the cheapest and the least exposed. The report places each of these precisely, with the valuation bridges.

And because a good thesis has to be falsifiable, the report runs the bear case in full rather than hiding it. Maybe this is a Peloton, a fad riding transient health anxiety, on “optimal ranges” that no major medical body has validated. Maybe the hardware commoditizes: Dexcom already sells an over-the-counter glucose sensor for 89 dollars a month, and if biomarkers get cheap at the pharmacy, the premium longevity club is hard to defend. We would change our minds if second-year retention on these platforms fell below 40 percent, if Apple or Google folded clinical-grade blood data into the phone for free, or if long studies showed that all this monitoring does not actually extend life.

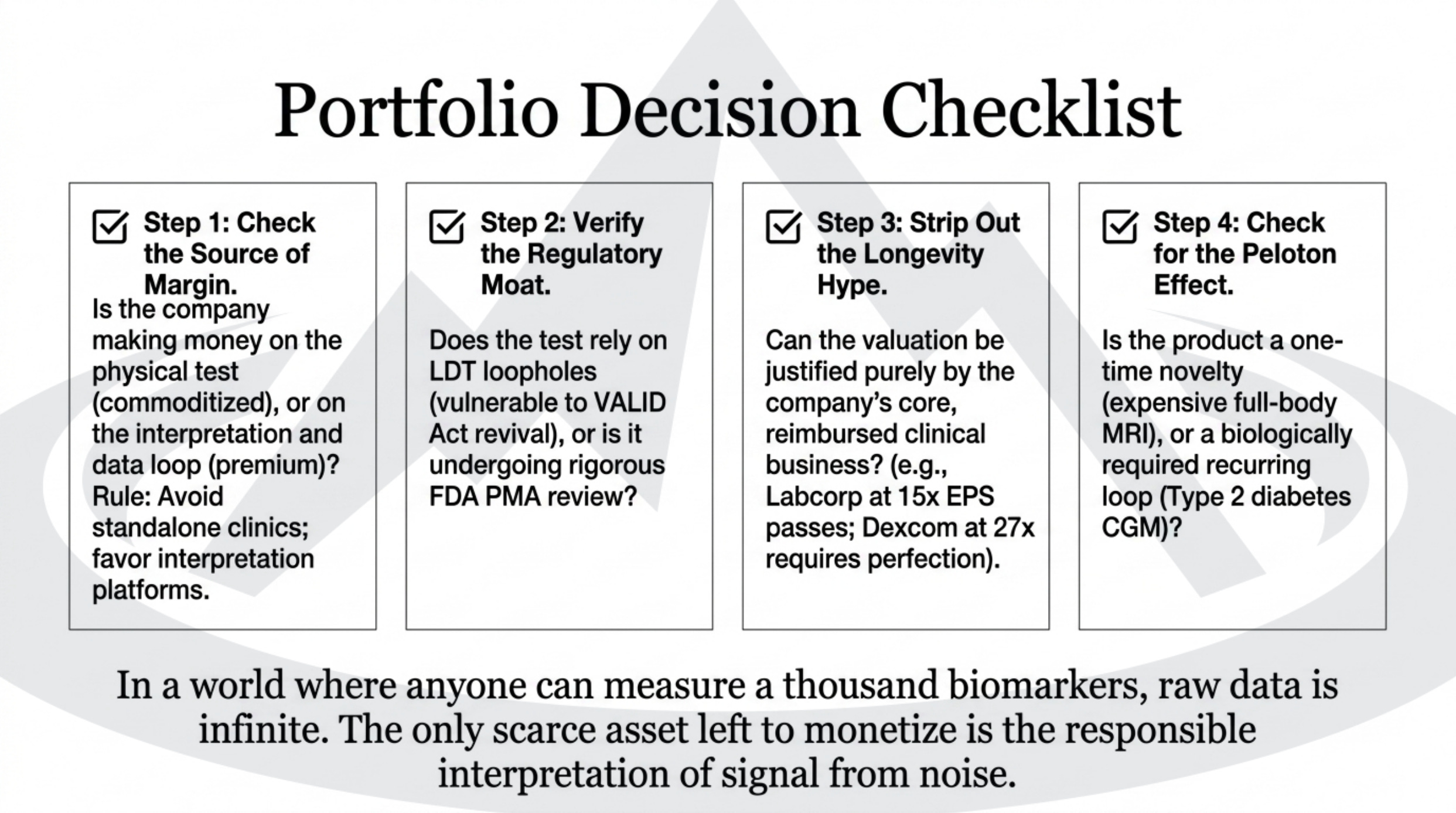

Which brings us back to the one line that survives the whole analysis. In a world where anyone can measure a thousand biomarkers, raw data is infinite, and infinite things are cheap. The only scarce asset left to monetize is the responsible interpretation of signal from noise. That is where the rent is, and that is what the full deep dive maps, nineteen pages of it: the value chain, the per-name valuation bridges, three scenarios to 2029, and the exact conditions that would prove us wrong. It is the desk’s work, and it is at moatpeak.com.

Educational research only. Not medical advice, and not personalised investment advice. MB “MoatPeak Group”.