The market isn't calm. It's pinned.

The stillness in this market is not the absence of risk. It is a machine. Today we open the hood: how the calm is manufactured, how to read it now, and the moment it turns violent.

Most people are reading the strange quiet in this market as a sign that everything is fine. We think that is exactly backwards, and today we want to open the hood all the way and show you the machine that manufactures the calm. Once you can see it, you cannot unsee it.

Start with the trade almost everyone is doing without realizing they are all doing it: selling volatility. It shows up in a hundred forms. Funds writing covered calls for income. Structured products that pay a yield in exchange for taking the other side of a market move. Systematic strategies that sell options because it has quietly been one of the best-paying trades of the decade. When all of that selling piles up, someone has to buy the other side, and that someone is the dealer.

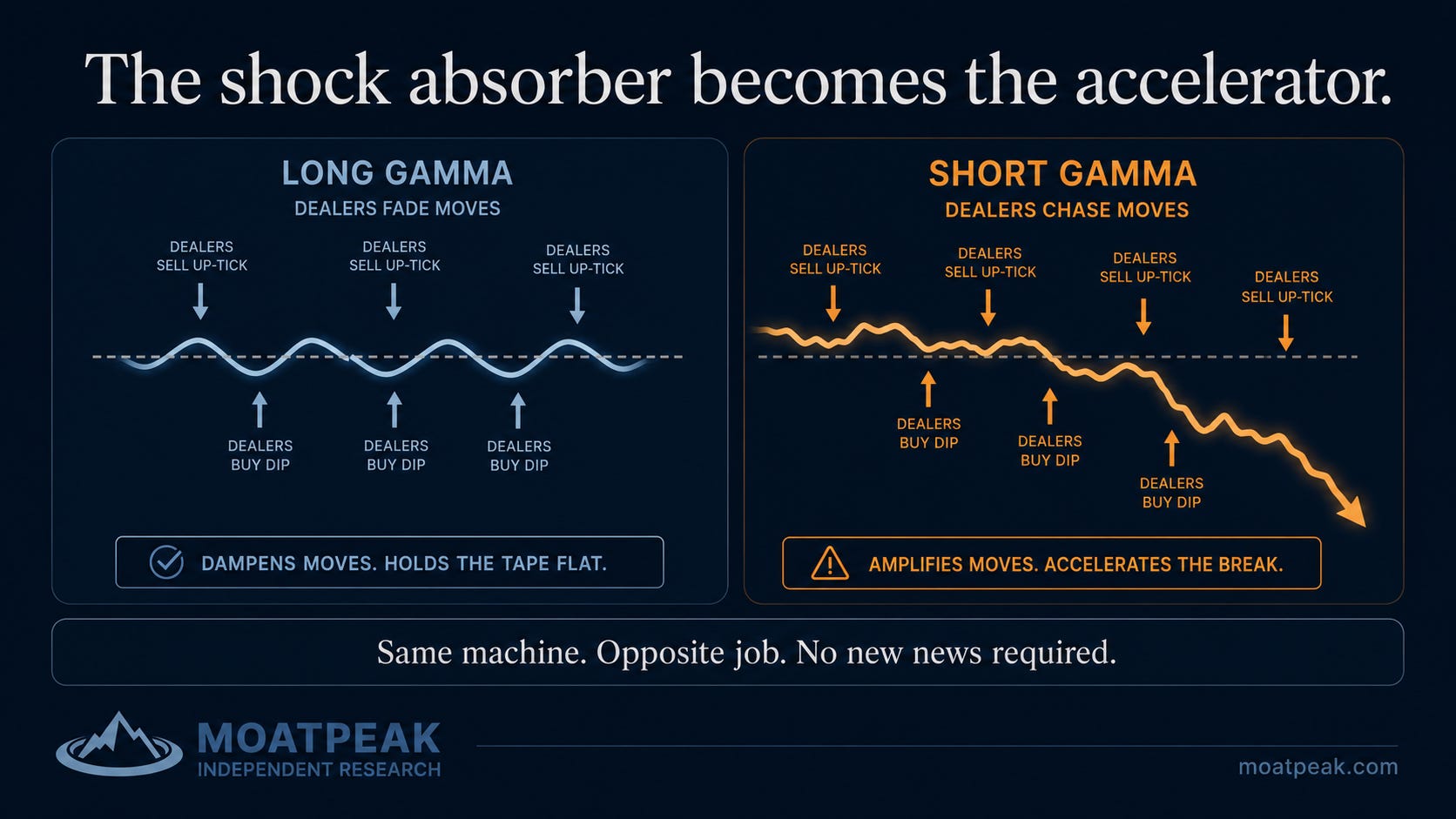

Here is the mechanical part that decides how the whole market behaves. When dealers are net buyers of options, they are what the trade calls long gamma, and to stay hedged they are forced to trade against every move the market makes. The index ticks up, they sell a little. It ticks down, they buy a little. They are not doing this because they have a view. They are doing it because their hedge demands it. Multiply that across the entire market and you get an invisible hand pressing the index flat all day, selling strength and buying weakness, smothering every attempt to move. The market is not calm because investors are relaxed. It is calm because it is being held in place.

And it feeds itself. Low volatility lets everyone run bigger positions on the same risk budget, which means more option-selling, which pushes volatility even lower, which invites even bigger positions. That is why these quiet regimes last far longer than anyone expects, and why they feel safest at the exact moment they are becoming the most dangerous.

Now the honest read on right now, with no pretending we can call the future. The market has spent recent sessions doing precisely this: grinding in a narrow band, volatility parked near its lows, and the correlation between stocks unusually depressed. That last point matters more than it sounds. When stocks stop moving together, a calm-looking index can be hiding real churn underneath, which means the headline quiet is understating how much is genuinely going on in individual names. The whole placid picture is resting on the belief that a particular recent low holds. As long as it does, the machine keeps humming and the range grinds gently higher. The positioning even tolerates a shallow dip, a small left tail the market has decided it can live with. None of that is a forecast. It is a description of the setup.

Here is what turns the shock absorber into an accelerator. If volatility spikes hard enough, the sellers of all those options start losing money faster than their risk limits allow, and they are forced to buy protection back. That flips the dealers from long gamma to short gamma, and now their hedge demands the opposite behavior: sell into weakness, buy into strength, in the same direction as the move. The exact machine that spent months absorbing every wobble suddenly starts amplifying it. No new information is required. A quiet tape can go violent purely because the positioning flipped. It is the same physics as portfolio insurance in 1987 and the short-volatility blow-up of early 2018: the machinery that manufactures the calm is the machinery that ends it.

So what do you actually watch, if not the headlines? Watch the things that would force the sellers to cover. A real jump in realized volatility, meaning how much the market is actually moving day to day, not just the headline fear gauge. Correlation rising, single stocks starting to move together again. And the level the whole calm is quietly defending, because a pin is only a pin until it is not. When a market goes eerily still, the question is never why is nothing happening. It is who is being paid to keep it this way, and what happens the day they cannot.

That is the honest picture of how this market is positioned. Not safe. Not fragile. Pinned. And a pin is a very particular kind of risk: quiet, cheap and comfortable, right up until the moment it is none of those things.

This is the kind of plumbing we spend our days inside. The daily read is the desk’s job at moatpeak.com.

Educational research only. Not investment advice. MoatPeak Group, UAB.