The most fragile thing in the market might be you.

Everyday investors now move the market more than ever. That's the good news. The tools they're using to do it are the bad news.

Here’s a genuinely new fact about markets, and it cuts both ways. The single most important buyer of US stocks is no longer a pension fund or some foreign giant. It’s the ordinary investor — you, your neighbour, the app in your pocket. Regular people now own more of the market, and move it more, than at almost any point in history. That’s a real democratisation, and mostly a good thing. But how that money is being put to work is where the story turns uncomfortable.

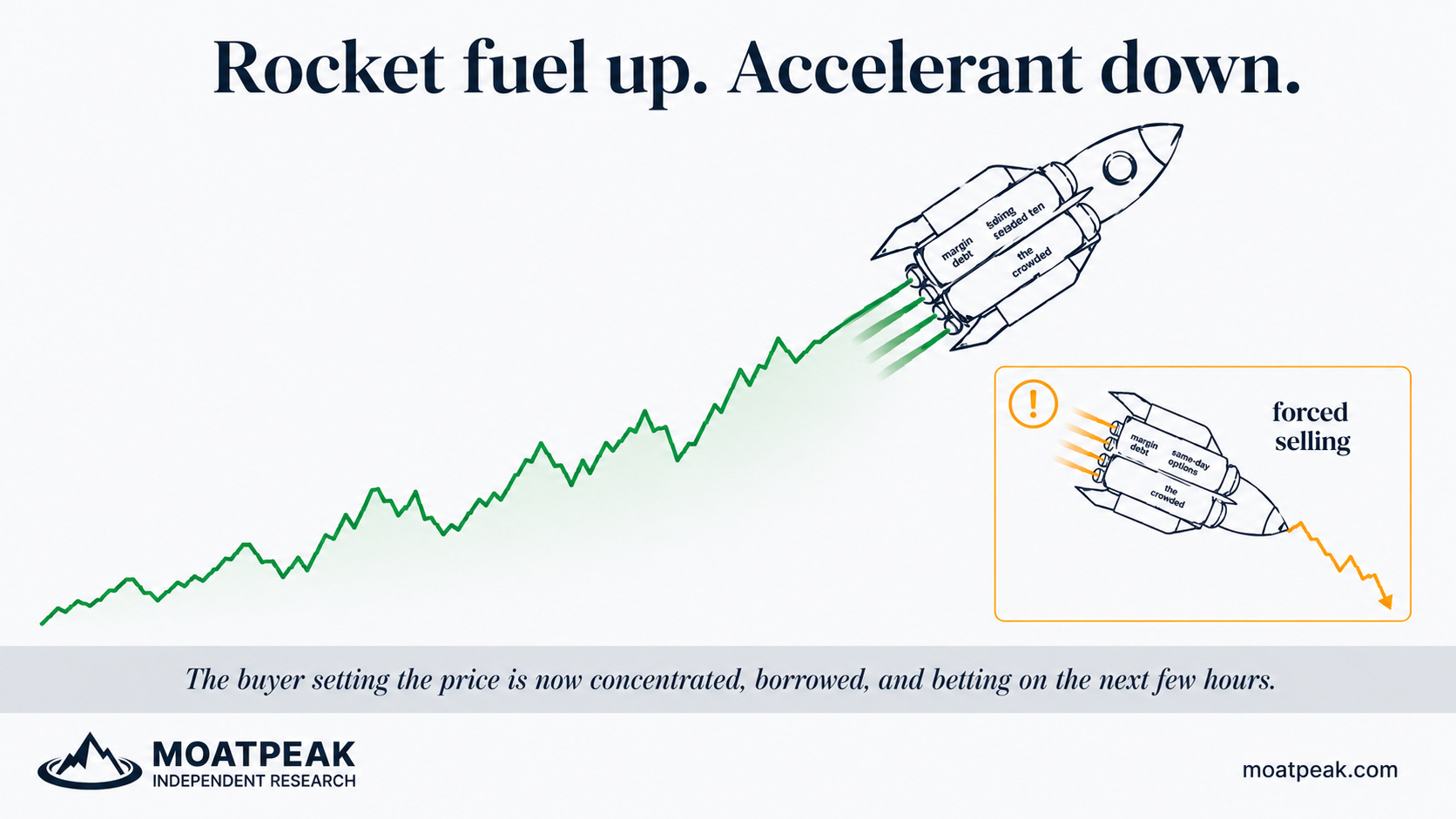

Start with borrowing. The amount investors have borrowed against their portfolios to buy yet more stock — the thing called margin debt — is at an all-time high, and it has been setting fresh records month after month. On its own, that’s just a big number. What makes it worth a second look is its history: this kind of borrowing tends to swell fastest right before the market’s worst moments. It ballooned into the dot-com top in 2000, into 2007, into the 2021 peak. Leverage is wonderful on the way up, because it multiplies your gains — and merciless on the way down, because when prices fall the borrowed money still has to be repaid, usually by selling at the exact worst moment. Borrowing to buy doesn’t add strength. It winds a spring, tighter the higher things climb.

Then there’s the newer wrinkle: options, and specifically the very short-dated kind. A huge and fast-growing share of all options now expire the same day they’re bought — bets, essentially, on where a stock lands in the next few hours. They’re cheap, they’re thrilling, and they’ve gone from a niche corner to something like half of all options activity. Most of that flow is calls: bets that things keep going up. Used carefully and sparingly, options are a legitimate tool. Used this way, at this scale, they start to look like scratch cards with a ticker printed on them — a great many small, fast, borrowed bets all pointing the same direction.

Put the two together and you’ve found the market’s hidden fault line. The buyer setting the price at the margin is now concentrated (piling into the same few names), borrowed (margin debt at records), and impatient (wagering on the next few hours). That mix is glorious in a calm uptrend: everyone leans the same way and the rally feeds itself. But it’s brittle. When the mood flips even slightly, the leverage forces selling, the same-day bets detonate, and everyone lunges for the same small exit at once. It’s why the market can now suffer a violent, two-day air-pocket with no recession behind it, no crisis, nothing “fundamental” at all — just the machinery of crowded, borrowed, short-dated money unwinding on itself.

None of this is a prediction that the roof is about to cave in, and none of it is a lecture about staying out of the market. It’s a quieter point, aimed squarely at your own account. The very forces that make the whole market fragile — leverage and same-day bets — are the ones most likely to quietly wreck an individual portfolio, and they’re being sold harder than ever as the fast lane to getting rich. The biggest edge a regular investor actually has isn’t a clever options play. It’s the ability to not become a forced seller — to own things you can hold straight through an air-pocket, without a margin call or an expiring bet making the decision for you. In a market running on borrowed time, patience isn’t the boring option. It’s the whole advantage.

Free weekly letter and explainers like this; the daily research, levels and the Daily Compass are at moatpeak.com.

Educational research only — not investment advice. MoatPeak Group, UAB.