The stock market votes on the story. The bond market votes on the bill.

Every big company is priced twice a day by two crowds that barely speak to each other. Right now they're telling opposite stories about AI — and the quieter one is worth more of your attention.

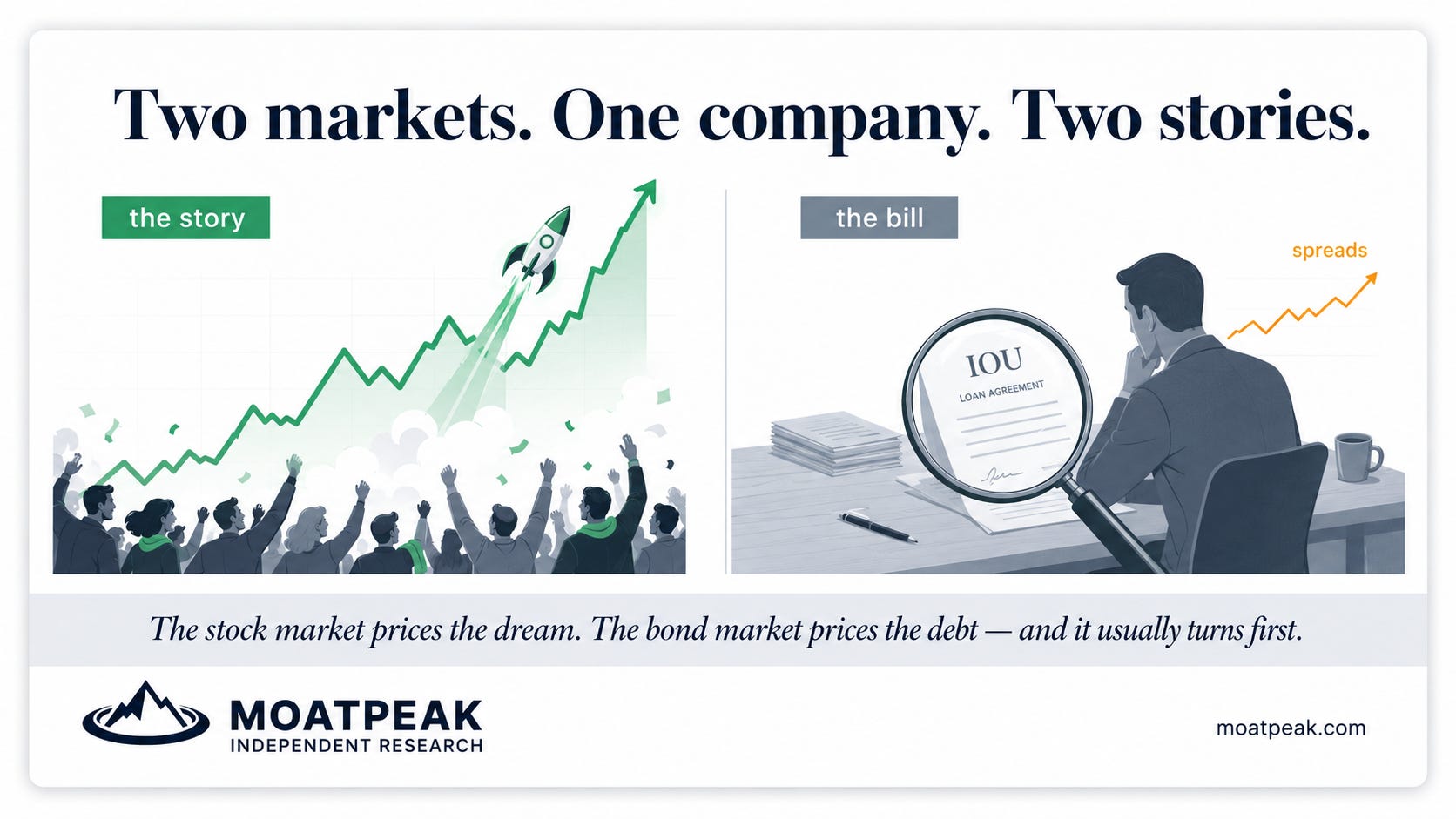

Every large company is priced twice over, every single day, by two different crowds who barely talk to one another. One is the stock market — loud, emotional, endlessly focused on how enormous the upside might be. The other is the bond market: the people who lent the company money. They get none of the upside, and they care about exactly one thing — will I be paid back? Those two crowds are currently telling very different stories about the great AI build-out, and knowing how to hear both is one of the more useful skills a regular investor can pick up.

The stock market’s version you already know by heart: euphoria, then a violent two-day wobble, then a bounce, repeat. But look instead at what the lenders have been doing, because it’s genuinely unusual. The handful of giants building out AI have been borrowing at a pace that broke what investors had literally treated as an unspoken contract — the understanding that these fortress-balance-sheet companies funded themselves out of profits, not debt. That understanding is gone. They’re now issuing bonds by the hundreds of billions to pay for a build-out large enough to swallow almost all the cash they generate, with more still to come.

Here’s the strange part, and the actual signal. Even as that borrowing has exploded, the extra interest that lenders demand for holding the debt sits near the lowest it has ever been. Record borrowing, met with record calm. Sit with how odd that pairing is. When a company borrows dramatically more and its lenders simply shrug, only two things can be true: either the lenders are genuinely certain nothing can go wrong, or they’re asleep at the wheel. History is not kind to the second possibility — and it’s the bond market, not the stock market, that has tended to wake up first at the big turning points.

Why would the lenders know first? Because of what a lender is. A shareholder is buying a dream; their imagination runs to the upside. A lender has no upside at all — the very best case is “I get my money back, with a little interest.” So lenders pour all their attention into the downside, into the single question that actually decides a company’s fate: can it pay its bills? They also stand ahead of shareholders in the queue if things go wrong. A crowd with a senior claim and no reason on earth to be optimistic makes for a very good early-warning system. When the people who only care about being repaid start to fidget, it means more than when the people dreaming of riches start to cheer.

And you don’t have to trade a single bond to use any of this. There’s a tell sitting in plain sight, and it’s free: the cost of insuring the biggest AI borrowers’ debt against default, and the gap between what their bonds pay and what safe government bonds pay. If those keep quietly creeping upward while the stocks keep ripping, the two markets are pulling apart — and the one to believe is the one with the senior claim and the longer memory. You’re not predicting a crash by watching it. You’re just refusing to listen to only the louder of two voices.

The stock market is voting on how good the story is. The bond market is voting on whether the story can pay for itself. Most of the time they agree and it doesn’t matter. It’s when they disagree that you want to remember which vote eventually gets counted.

Free weekly letter and explainers like this; the daily research, levels and the Daily Compass are at moatpeak.com.

Educational research only — not investment advice. MoatPeak Group, UAB.