The whole market is two stocks right now.

The number everyone will cheer this week hides two things: the strong market is really two chip stocks, and the fear about it is now the most crowded trade of all.

This week the market meets its referee. Earnings season opens with a wall of banks, then the two names that matter most for the whole story, TSMC and ASML. And the number everyone will read out is that S&P 500 profits are set to grow somewhere around 22 percent. Said out loud, that sounds like a strong economy and a strong market, broad and healthy. It is one of the most misleading true numbers you will hear all year.

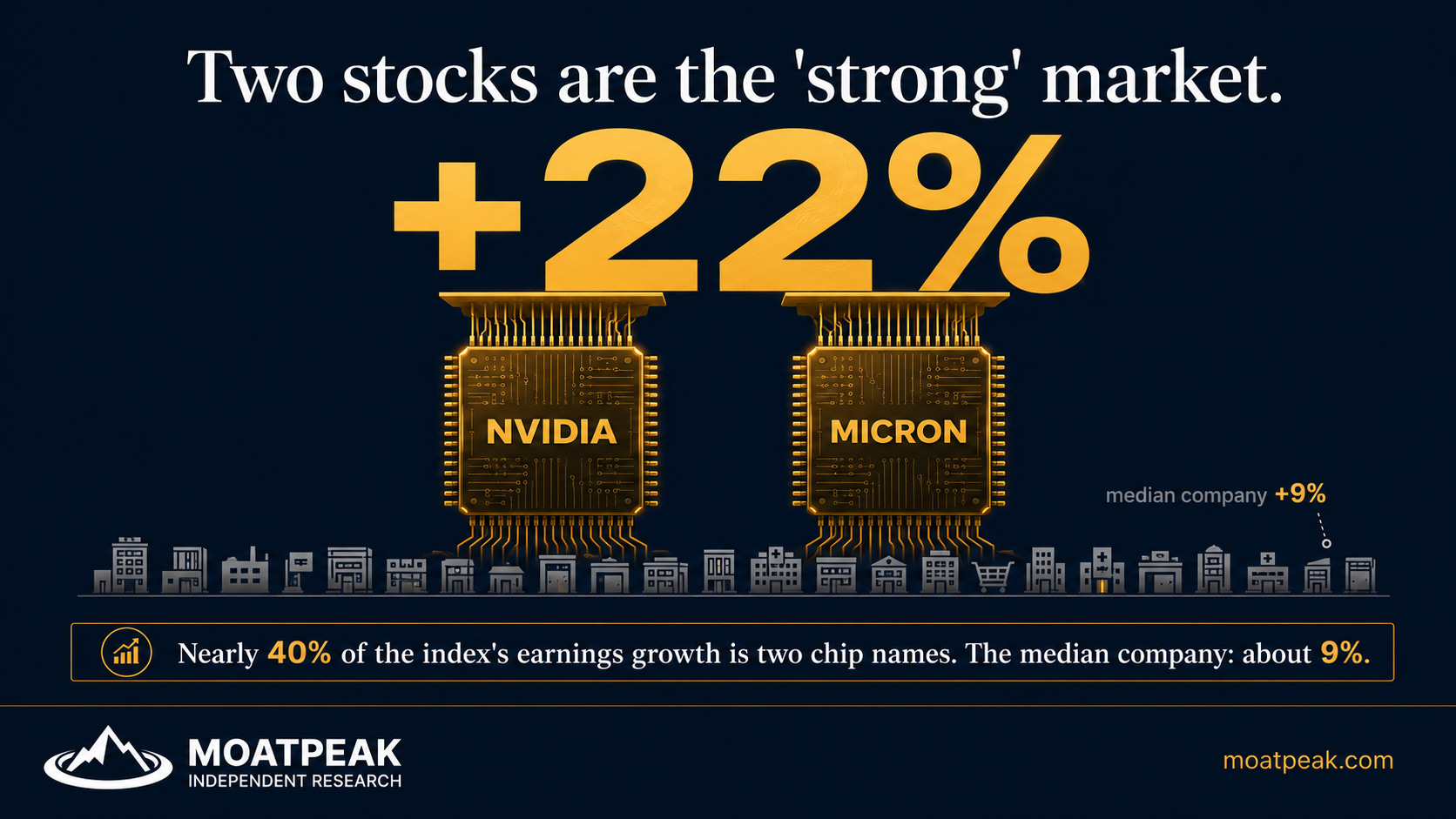

Here is what that 22 percent is actually made of. Strip the index back to the typical company and the median business in the S&P 500 is growing earnings around 9 percent. Ordinary. The gap between that 9 and the headline 22 is not spread across the market. It is a handful of AI names, and at the very center of it, close to 40 percent of the entire index’s earnings growth this quarter comes from just two chip stocks: Nvidia and Micron. Micron alone is putting up growth in the four figures. So when the anchors tell you corporate America is booming, be precise about what is booming. Two semiconductor companies are having a historic quarter. The other roughly 498 are having a normal one.

This matters because an index whose growth is 40 percent two names is not diversified earnings. It is a concentrated bet wearing a broad label. And it is a leveraged one. Margin debt, the money investors borrow to buy stocks, just hit a record 1.4 trillion dollars, up 54 percent in a single year, the fastest borrowing pace in about three decades, and it is pooled in the same small cluster of AI and chip names. Every major market peak of the past century topped out with a margin-debt record just like this one. So the beat this week is not enough on its own. Those two names do not just have to report a good quarter, they have to guide well enough to justify an enormous future spending bill, or a market priced for perfection re-rates hard. Two reports can move the entire index. The headline hides how narrow the floor really is.

Now here is the part almost nobody is saying, because it cuts against the mood. The fear about all of this has itself become the crowded trade. Step back from the stock market and look at how the professionals are positioned in interest rates, and you find the entire crowd leaning the same way: leveraged funds are sitting on a record short position in short-term rate futures, the most extreme in the history of the data, all betting that the Fed hikes and the squeeze keeps tightening. When everyone is braced in the same direction, the dangerous move is the other one. A single soft inflation print, or a Fed that simply does nothing, could force all of those shorts to cover at once and fire a violent relief rally in exactly the assets everyone is positioned against. The crowd is no longer greedy. It is scared. And a crowded fear is every bit as dangerous as a crowded greed.

So put the two halves together and you get the honest picture of this week, and it is genuinely two-sided. The market’s growth is borrowed from two stocks, which makes the confident bull case more fragile than the 22 percent headline suggests. But the fear is one-way and crowded, which makes the confident bear case more dangerous than the doom suggests. This is the trap at both ends. The people certain it is fine are leaning on two chip reports. The people certain it is over are standing in the most crowded short in years.

The useful move, as ever, is not to pick a mob. It is to know which one you are quietly standing in, and to watch the two things that actually settle it: whether those two names guide strongly enough to justify the spend, and whether the crowd braced for disaster gets squeezed first. Read the verdict this week. Do not front-run it. And never again mistake a loud headline number for a broad one.

This is the kind of thing we take apart every day, in the open. The full daily read is the desk’s job at moatpeak.com.

Educational research only. Not investment advice. MB “MoatPeak Group”